|

When Covid first struck I took a cautious approach, turning many of my investments into cash. Then the massive fiscal, monetary and, later, the vaccine stimuli came to the fore and I turned buyer. Here is a list of all the shares I’ve bought and written about on ADVFN in the Covid period. I’ve been fortunate.

Company Purchase date Purchase price Divs to 31.3.21 Price 31.3.21 Return to 31.3.212021 Connect (Smiths News)18.3.20 £0.151 zero £0.365 142% Character 5.6.20 £2.52 5p £4.50 81% McCarthy & Stone 1.10.20 £0.718 0 Sold 7.12.20 £1.185 65% Cap|Co 6.11.20 £1.032 0 £1.714 66% Dewhurst “A” 11.11.20 £5.94 9.25p £7.00 19% MS International 16.12.20 £1.292 1.75p £1.60 25% Wynnstay 29.12.20 £3.405 zero £4.80 41% Lloyds Bank 12.3.21 £0.4169 zero £0.427 2% J Smart 18.3.21 & 24.3.21 £1.253 zero £1.22 -3%Longer run performance Almost eight years ago that I left a tenured professorship to concentrate on investment. Back then the FTSE 100 was around 6,600. It is now 6,900 – a slow rise but there have been dividends of around 3-4% per year. I believe the numbers in the tables below show that I have outperformed, which is quite a relief given the salary and security sacrifice I made almost eight years ago. The tables show the results (so far) of all the shares bought for the portfolios I’ve been writing about in my Newsletters. The comments I made at the time explaining the rationale for each investment are available for you to read in older newsletters - there is nowhere for me to hide from my appraisals I made three, four or seven years ago – all the errors of omission and commission are there in broad daylight. I present the returns after taking the hit on broker costs, stamp duty and bid/offer spread. (Some of you have joined us recently so, in case you are not familiar with them, I briefly describe the criteria for my portfolios following the portfolio performance tables.) The 2013 Net Current Asset Value, NCAV, portfolio Company Purchase date Purchase price Divs to 31.3.21 Price 31.3.21 Return to 31.3.21 French Con.25.7.13 £0.3047 zero Sold July15 £0.4378 44% Caledonian T 25.7.13 £0.70 zero Sold April20 £1.391 99% Fletcher King 6.8.13 £0.30 14.25p Sold June16 46p 101% Northamber 22.8.13 £0.287 1.6p Sold Oct16 £0.303 11% Titon 5.9.13 £0.379 6.5p Sold May16 £1.06 197% Mallett 12.11.13 £0.7682 12.7p Sold Nov14 £0.60 -5% AVERAGE 75%The 2014 NCAV portfolio Company Purchase date Purchase price Divs to 31.3.21 Price 31.3.21 Return to 31.3.21 Holders Tech 10.10.14 & 3.11.14 £0.47 1p Sold Mar17 £0.33 -28% Airea 4.11.14 £0.1195 0.9p Sold Sept16 £0.309 166% Northamber 17.11.14 £0.4265 0.7p Sold Oct16 £0.303 -27% Caledonian T 30.12.14 £1.39 zero Sold April20 £1.391 0 AVERAGE 28%The 2015 NCAV portfolio Company Purchase date Purchase price Divs to 31.3.21 Price 31.3.21 Return to 31.3.21 PV Crystalox 15.1.15 £0.122 zero Sold Dec16 £0.237 94% Arden Partners 1.9.15 £0.422 1p Sold May18 £0.364 -11% Northamber 4.9.15 £0.443 0.4p Sold Dec16 £0.303 -31% AVERAGE 17%The Buffett-style portfolio This type of share is rarer than the others, and so I combine all years. Company Purchase date Purchase price Divs to 31.3.21 Price 31.3.21 Return to 31.3.21 Dewhurst 9.4.14 £3.18 70.5p Sold Feb20 £7.217 149% MS International 9.10.19 £1.723 5.25p £1.60 -4% Character 20.1.20 & 5.6.20 £2.811 13p £4.50 65% Dewhurst 11.11.20 £5.94 9.25p £7.00 19% MS International 16.12.20 £1.292 1.75p £1.60 25% AVERAGE 51%(I bought some more of Dewhurst in June 2014 at £3.11, December 2014 at £3.75, November 2017 at £5.46, February 2019 at £5.54 and April 2019 at £5.64.These were sold Feb 2020). Modified price earnings ratio portfolio 2015/16 Company Purchase date Purchase price Divs to 31.3.21 Price 31.3.21 Return to 31.3.21 Haynes 11.2.15 £1.159 33.5p Sold 2.10.19 £2.9175 181% AGA 11.3.15 £1.002 zero Taken over June 2015 £1.456 45% Hogg Robinson 10.4.15 £0.4709 2.37p Sold June 2016 £0.656 44% MS International 3.7.15 £1.86 37.75p £1.70 12% BHP Billiton 24.9.15 £10.43 127p Sold May 2018 £16.90 74% TClarke 5.11.15 £0.7916 13.61p Sold Feb 2020 £1.1215 59% Premier Farnell 8.4.16 £1.222 3.6p Taken over 20.6.16 £1.632 36% AVERAGE 64%The AGA holding was doubled 30 April 2015 at a price of £0.9466. Modified price earnings ratio portfolio 2017 CompanyPurchase.................To read more subscribe to my premium newsletter Deep Value Shares – click here http://newsletters.advfn.com/deepvalueshares/subscribe-1

0 Comments

Seven and a half years ago that I left a tenured professorship to concentrate on investment. Back then the FTSE 100 was around 6,600. The market as a whole has not exactly moved strongly in a positive direction over that time. It is now 6,620 (although there have been dividends of around 3-4% per year).

Despite this, I suppose I can be pleased with my performance so far, especially in light of the fact that my approach – deep value – generally has not done well in an era of great excitement about growth companies. The remarkable downs and ups of this year were a challenge for all investors. Caution was the watchword in February and March when I sold a number of companies vulnerable to deep recession to raise cash for a hunkering down. Out went Dewhurst (at 722p, now 600p), T Clarke (at 112.15p, now at 95.4p), Northamber (at 57.2p, now at 52p) J Smart (at 110p, now at 110p) Caledonian Trust (at 139.1p, now at 140p). Having built up cash reserves I was ready to look for bargains in the panic - always “look for opportunity in the flux”. The first I found was Connect Group (recently renamed Smith News) where I doubled my holding at a price of 15.1p. These shares are now trading at 28.1p. Then I doubled my holding of Character Group in June at 252p. These now trade at 410p. I had to wait until October before I felt ready to gain exposure to the property sector again. But the attractive net current asset value, NCAV, of McCarthy and Stone was just too tempting. Even if the recession turned out to be prolonged this company had so many assets, and manageable debt, that it was a bargain at 71.8p. It wasn’t long before an American private equity company concluded that it was a good business packed with assets, and made a takeover bid at 120p per share. I sold out in early December at 118.5p, a return of 65% in two months. Then there was the owner of Covent Garden, Capital and Counties Properties, which Mr Market had dumped alongside other office and shop owners. It was selling far below its NCAV, even taking a pessimistic line on where property prices were going. But Covent Garden is not like other shopping/office/leisure areas, being dominated by tourism and activity in central London. I thought it would bounce back sooner or later, so I bought at 103.2p. Low and behold, my timing was perfect (pure luck) I bought on the Friday (6th Nov) and on the Monday the Pfiser vaccine was approved resulting in estimates of future footfall within London being revised upward. It is now trading at 144.4p. These two investments demonstrate the benefits of deep value investments: you don’t know what is going to correct the under-pricing – a takeover bid, a management revamp, Mr Market switching from pessimism to optimism, or the liquidation of a competitor – nor when it will occur, but you do know (probably) that one day it will rise to somewhere near intrinsic value. So, all you have to do is estimate intrinsic value, compare that with what the market is asking for the shares, see if there is a good margin of safety and be bold in buying. And be bold in selling. I sold Tandem in August at 370.7p when I was still pretty nervous about the economic outlook and after it had risen to give a 139% return. It was not that I was pessimistic about the company, just that I was concerned that things might go wrong at the company (bicycle enthusiasm has pushed this one up, despite it losing money in its bicycle division for years and having difficulty sourcing bikes to sell in the UK). In hindsight I should have let the share run because it rose above 550p. I comfort myself with the thought that much of the money raised went into McCarthy and Stone and Covent Garden. The money also went into buying back into, and purchasing more of, Dewhurst “A” shares at a price much lower than I sold in February - sold at 722p, bought back at 594p. Very recently I’ve more than doubled my holding in MS International at 129.2p and tripled my Wynnstay holding at 340.5p – I’ll set out my reasoning in a set of Newsletters soon. The Deep Value Strategy performance tables The results (so far) of all the shares bought for the portfolios I’ve been writing about in my Newsletters are shown in the tables below. The comments I made at the time explaining the rationale for each investment are available for you to read in older newsletters - there is nowhere for me to hide from my appraisals made three, four or seven years ago. I present the returns after taking the hit on broker costs, stamp duty and bid/offer spread. (Some of you have joined us recently so, in case you are not familiar with them, I briefly describe the criteria for my portfolios following the portfolio performance tables.) The 2013 Net Current Asset Value, NCAV, portfolio Company Purch date Purch price Divs to 31.12.20 Price 31.12.20 Return to 31 December 2020 French Con.25.7.13 £0.3047 zero Sold July 2015 £0.4378 44% Caledonian T25.7.13 £0.70 zero Sold April 2020 for £1.391 99% Fletcher King6.8.13 £0.30 14.25p Sold June 2016 for 46p 101% Northamber22.8.13 £0.287 1.6p Sold Oct 2016 £0.303 11% Titon5.9.13 £0.379 6.5p Sold May 2016 £1.06 197% Mallett12.11.13 £0.7682 12.7p Sold Nov 2014 £0.60 -5% AVERAGE 75% The 2014 NCAV portfolio Company Purchase date Purchase price Divs to 31.12.20 Price 31.12.20 Return to 31 12.20 Holders Tech10.10.14 & 3.11.14 £0.47 1p Sold March 2017 £0.33 -28% Airea4.11.14 £0.1195 0.9p Sold Sept 2016 £0.309 166% Northamber17.11.14 £0.4265 0.7p Sold Oct 2016 £0.303 -27% Caledonian T30.12.14 £1.39 zero Sold April 2020 for £1.391 0 AVERAGE 28% The 2015 NCAV portfolio Company Purchase date Purchase price Divs to 31.12.20 Price 31.12.20 Return to 31.12.20 PV Crystalox 15.1.15 £0.122 zero Sold Dec 2016 £0.237 94% Arden Partners 1.9.15 £0.422 1p Sold May 2018 £0.364 -11% Northamber 4.9.15 £0.443 0.4p Sold Dec 2016 £0.303 -31% AVERAGE 17% The Buffett-style portfolio This type of share is rarer than the others, and so I combine all years. Company Purchase date Purchase price Divs to 31.12.20 Price 31.12.20 Return to 31.12.20 Dewhurst 9.4.14 £3.18 70.5p Sold February 2020 £7.217 149% MS International 9.10.19 £1.723 3.5p £1.15 -31% Character 20.1.20 & 5.6.20 £2.811 15p £4.10 51% Dewhurst 11.11.20 £5.94 0 £6.00 1% MS International 16.12.20 £1.292 0 £1.15 -11% AVERAGE 40% (I bought some more of Dewhurst in June 2014 at £3.11, December 2014 at £3.75, November 2017 at £5.46, February 2019 at £5.54 and April 2019 at £5.64.These were sold Feb 2020). Modified price earnings ratio portfolio 2015/16 Company Purchase date Purchase price Divs to 31.12.20 Price 31.12.20 Return to 31.12.20 Haynes 11.2.15 £1.159 33.5p Sold 2.10.19 £2.9175 181% AGA 11.3.15 £1.002 zero Taken over June 2015 £1.456 45% Hogg Robinson 10.4.15 £0.4709 2.37p Sold June 2016 £0.656 44% MS International 3.7.15 £1.86 36p £1.15 -19% BHP Billiton 24.9.15 £10.43 127p Sold May 2018 £16.90 74% TClarke 5.11.15 £0.7916 13.61p Sold Feb 2020 £1.1215 59% Premier Farnell 8.4.16 £1.222 3.6p Taken over 20.6.16 £1.632 36% AVERAGE 60% The AGA holding was doubled 30 April 2015 at a price of £0.9466. Modified price earnings ratio portf ………………To read more subscribe to my premium newsletter Deep Value Shares – click here http://newsletters.advfn.com/deepvalueshares/subscribe-1 Investors need to be cautious in supporting directors of their companies when pursuing the purchase of other firms. It's well-known that most mergers/acquisitions fail to produce shareholder value. This newsletter looks at the principles Buffett follows to improve the odds of success. He set these down for us shortly after buying Helzberg Diamonds in 1995.

Acquisition by walking around On a sunny May morning a week or so after Berkshire’s 1994 annual meeting in Omaha, Warren Buffett was about to cross near the corner of 58th Street and Fifth Avenue New York when he was stopped by a woman who just wanted to say how much she had enjoyed the Annual Meeting. Barnett C Helzberg, Jr, who was in New York to talk to Morgan Stanley about, possibly, selling his business, a 143 jewelry store chain carrying his family name, was 30-40 feet away when the woman in the bright red dress shouted across to Buffett. On hearing the name of the chairman of the company in which he held four shares he stopped and waited for the woman to say her goodbyes. As Buffett went to cross the street – again - Helzberg saw his opportunity. He thrust out his hand, “Hello, Mr. Buffett. I’m Barnett Helzberg of Helzberg Diamonds in Kansas City” (Barnett Helzberg, Jr. (2003) “What I Learned Before I Sold to Warren Buffett: An Entrepreneurs Guide to Developing a Highly Successful Company” John Wiley & Sons). Helzberg looked for some recognition on Buffett’s face. But none was forthcoming, despite Helzberg then being one of the largest jewelry chain in the country. But Buffett was polite and shook his hand, said “Hello” and graciously accepted more compliments about the Annual Meeting. Then, in 30 seconds flat, “right there on the sidewalk, as busy New Yorkers rushed past us and street traffic buzzed around us, I told one of the most astute businessmen in America why he ought to consider buying our family’s 70-year-old jewelry business…I believe that our company matches your criteria for investment.” As Buffett recalls the encounter his first thought was that he was hearing yet again that phrase about a “good fit” when the business hawker hasn’t really understood the acquisition criteria applied by Buffett and Munger, “it usually turns out they have a lemonade stand - with potential, of course, to quickly grow into the next Microsoft.” (Buffett's 1995 letter to Berkshire shareholders) Given the probability that this was yet another dead end Buffett cut short the conversation by civilly asking if Helzberg could write to him with the particulars, “that, I thought to myself, will be the end of that.” Helzberg went home and sent Buffett nothing. He later said he was “afflicted by hang-ups about confidentiality. I’m the kind of guy who asks for someone’s Social Security number before I tell them the time.” Then one night he re-read Berkshire’s Annual Report and paid particular attention to the section where Buffett invites companies that meet his criteria to send him information. Buffett’s acquisition criteria Here is the regular “advertisement” included in Berkshire annual reports (this one is from 1995): “We are eager to hear from principals or their representatives about businesses that meet all of the following criteria: (1) Large purchases (at least $25 million of before-tax earnings), (2) Demonstrated consistent earning power (future projections are of no interest to us, nor are "turnaround" situations), (3) Businesses earning good returns on equity while employing little or no debt, (4) Management in place (we can't supply it), (5) Simple businesses (if there's lots of technology, we won't understand it), (6) An offering price (we don't want to waste our time or that of the seller by talking, even preliminarily, about a transaction when price is unknown). The larger the company, the greater wi………………To read more subscribe to my premium newsletter Deep Value Shares – click here http://newsletters.advfn.com/deepvalueshares/subscribe-1 It’s important at this time of enormous economic threat to listen to people who possess, through decades of intellectual effort, an informed long-term perspective on markets. I’ve been reading recent work by James Montier, Andy Haldane and Warren Buffett.

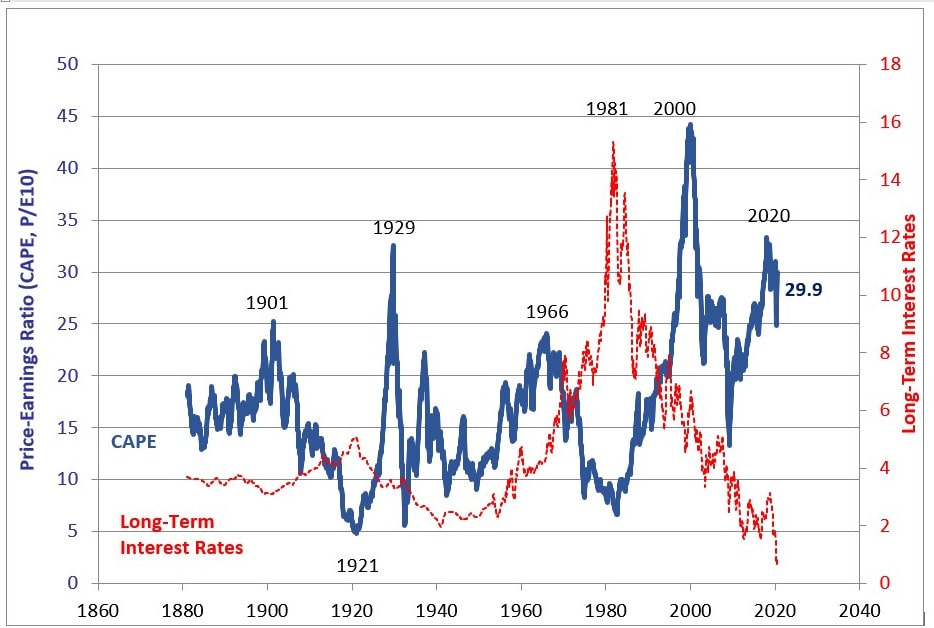

In today’s newsletter I’ll try to summarise James Montier’s views on the American market. James has written insightful articles for decades based on meticulous research. He worked as a Global Strategist at Société Générale before joining the thought-powerhouse and leading investment manager GMO. Apart from his articles, he has written important books such as Behavioural Investing and Value Investing. His knowledge base stretches from academic research on market out-performance through the psychology of investors to stock market history and the usefulness of valuation metrics (I recommend his books and his articles to you, many of which are available free on GMO’s website). Montier thinks the US equity market has moved into “absurd” territory. It is close to its highest price ever relative to fundamentals such as earnings at exactly the time that it is facing one of the worst economic downturns. It is just not allowing for the possibility of there being a downside – everything is rosy – the market is priced for a perfect business future. The odds of perfection being attained are not good. My next newsletter considers Andy Haldane’s ideas on where the UK economy has got to. Haldane is the Bank of England’s Chief Economist and was recently in the headlines for saying that the V-shaped recovery was underway. What he actually said was rather more subtle than what the newspaper writers described. Many scribblers took him to mean that the V was pretty well complete; we’re all going to get back to normal soon. Sadly, for businesses, the unemployed and the soon to be unemployed that just is not where we are. The V is far from complete on the right-hand side. It may not be for a long time yet. Finally, Warren Buffett has made a lot of large share stake sales in the last six months. For example, all Berkshire’s holdings of Goldman Sachs and JP Morgan have been sold, along with all its airline stocks. Billions have been raised from selling down Wells Fargo, US Bancorp and Bank of NY Mellon. During the same period Berkshire’s cash balance has grown to $143bn (yes, that is billion, not million) and Japanese trading house and Barrick Gold shares have been bought. What is Warren, through his actions, telling us about the future? James Montier - a Panglossian US equity market James Montier (in Reasons (NOT) To Be Cheerful, available at GMO’s website) is not focused on predicting the near- or medium-term future of the US equity market. He is more refined than that. He is using the data we have to point out that current prices are not allowing sufficiently for the potential of bad outcomes “It is as if Mr. Market is taking a tail risk (albeit a good one) and pricing it with certainty.” What James is saying is that there is a range of alternative futures, as there is at any point in history. We simply do not know which course will be taken. If the possibilities are potted on a graph with, on the x-axis showing increasingly bad results on the left of the centre, and increasingly good results on the right, and the probability of those outcomes occurring on the y-axis, the “shape” of the distribution could be “bell-shaped”. That is, the outcomes near the middle have the highest chance of occurring, while the extremes – the tails - have low probabilities. The extremes might contain scenarios such as a depression worse that of the 1930s on the left and, on the right, economic growth of 2%, or 3%, or 4% per year for the next few years. What James is saying is that the extreme good economic outcomes are the ones Mr Market is placing all his money onto. Investors have bid up share prices so much that they are at record or near record levels relative to rational measures of value. “Never before have I seen a market so highly valued in the face of overwhelming uncertainty. Yet today the U.S. stock market stands at nosebleed-inducing levels of multiple, whilst the fundamentals seem more uncertain than ever before. It appears as though the U.S. stock market has drunk from Dr. Pangloss’ Kool-Aid – where everything is for the best in the best of all possible worlds.” James says he doesn’t know what the outcome will be, whether there will be a second Covid-19 wave, or we’ll get the unemployed back to work quickly, etc., but he knows downside risks exist and therefore we should be demanding a margin of safety when we pay for a share - “wriggle room for bad outcomes if you like.” Mr. Market is not allowing for that margin of safety. What is Mr Market thinking? A major preoccupation for the generality of US investors/punters is the support to businesses and the economy provided by the Federal Reserve in supplying oceans of liquidity – basically pumping in money. But Montier points out, much of this involves banks swapping holdings of say long-term Treasury bonds for short term deposits at the central bank and is therefore not directly stimulating the equity markets, even if the thought of the Fed helping out is encouraging investors to buy. Besides, quantitative easing has also been strong in Europe and elsewhere but equity markets there are not “sporting extreme valuations”. “So, I think that Fed-based explanations are at best ex post justifications for the performance of the stock market; at worst they are part of a dangerously incorrect narrative driving sentiment (and prices higher)…The U.S. stock market looks increasingly like the hapless Wile E. Coyote, running off the edge of a cliff in pursuit of the pesky Roadrunner but not yet realizing the ground beneath his feet had run out some time ago.” James quotes Voltaire, “ ‘Doubt is not a pleasant condition, but certainty is absurd.’ The U.S. stock market appears to be absurd.” Overconfidence and overoptimism Overconfidence and overoptimism are………………To read more subscribe to my premium newsletter Deep Value Shares – click here http://newsletters.advfn.com/deepvalueshares/subscribe-1 It has been a tumultuous few months on the markets. To protect the downside risk I sold a number of investments in the winter and early spring, particularly those associated with creating, maintaining or holding property:

Thus, I have shifted the portfolio to hold more cash. However, there were two opportunities to buy which I couldn’t resist:

In January I bought into the deep value investment of Wynnstay, a farm supplies company, at £3.173. The tables below show the results (so far) of the shares bought for the portfolios I’ve been writing about in my Newsletters. The comments I made at the time explaining the rationale for each investment are available for you to read in older newsletters - there is nowhere for me to hide from my appraisals made three, four or five years ago. I present the returns after taking the hit on broker costs, stamp duty and bid/offer spread. My first purchase was 25th July 2013 when the FTSE100 was at 6,620. It is now at 6,170. (Some of you have joined us recently so, in case you are not familiar with them, I briefly describe the criteria for my portfolios following the portfolio performance tables.) The 2013 NCAV portfolio CompanyPurchase date Purchase price Divs to 30 June 2020 Price 30 June 2020 Return to 30 June 2020 French Con.25.7.13 £0.3047 zero Sold July 2015 £0.4378 44% Caledonian T25.7.13 £0.70 zero Sold April 2020 for £1.391 99% Fletcher King6.8.13 £0.30 14.25p Sold June 2016 for 46p 101% Northamber22.8.13 £0.287 1.6p Sold Oct 2016 £0.303 11% Titon5.9.13 £0.379 6.5p Sold May 2016 £1.06 197% Mallett12.11.13 £0.7682 12.7p Sold Nov 2014 £0.60 -5% AVERAGE 75%The 2014 NCAV portfolio CompanyPurchase date Purchase price Divs to 30 June 2020 Price 30 June 2020 Return to 30 June 2020 Holders Tech10.10.14 & 3.11.14 £0.47 1p Sold March 2017 £0.33 -28% Airea4.11.14 £0.1195 0.9p Sold Sept 2016 £0.309 166% Northamber17.11.14 £0.4265 0.7p Sold Oct 2016 £0.303 -27% Caledonian T30.12.14 £1.39 zero Sold April 2020 for £1.391 0 AVERAGE 28%The 2015 NCAV portfolio CompanyPurchase date Purchase price Divs to 30 June 2020 Price 30 June 2020 Return to 30 June 2020 PV Crystalox15.1.15 £0.122 zero Sold Dec 2016 £0.237 94% Arden Partners1.9.15 £0.422 1p Sold May 2018 £0.364 -11% Northamber4.9.15 £0.443 0.4p Sold Dec 2016 £0.303 -31% AVERAGE 17%The Buffett-style portfolio This type of share is rarer than the others, and so I combine all years. CompanyPurchase date Purchase price Divs to 30 June 2020 Price 30 June 2020 Return to 30 June 2020 Dewhurst9.4.14 £3.18 70.5p Sold February 2020 £7.217 149% MS International9.10.19 £1.723 1.75p £1.21 -29% Character20.1.20 & 5.6.20 £2.811 13p £3.22 19% AVERAGE 46%(I bought some more of Dewhurst in June 2014 at £3.11, December 2014 at £3.75, November 2017 at £5.46, February 2019 at £5.54 and April 2019 at £5.64). Modified price earnings ratio portfolio 2015/16 CompanyPurchase date Purchase price Divs to 30 June 2020 Price 30 June 2020 Return to 30 June 2020 Haynes11.2.15 £1.159 33.5p Sold 2.10.19 £2.9175 181% AGA11.3.15 £1.002 zero Taken over June 2015 £1.456 45% Hogg Robinson10.4.15 £0.4709 2.37p Sold June 2016 £0.656 44% MS International3.7.15 £1.86 34.25p £1.21 -17% BHP Billiton24.9.15 £10.43 127p Sold May 2018 £16.90 74% TClarke5.11.15 £0.7916 13.61p Sold Feb 2020 £1.1215 59% Premier Farnell8.4.16 £1.222 3.6p Taken over 20.6.16 £1.632 36% AVERAGE 60%The AGA holding was doubled 30 April 2015 at a price of £0.9466. Modified price earnings ratio portfolio 2017 CompanyPurchase date Purchase price Divs to 30 June 2020………………To read more subscribe to my premium newsletter Deep Value Shares – click here http://newsletters.advfn.com/deepvalueshares/subscribe-1 A bleak economic outlook according to the Organisation for Economic Cooperation and Development23/6/2020 The Economic Outlook report published a couple of weeks ago predicts very poor prospects for most economies and businesses over the next two years.

It presents two possible scenarios: one where the virus continues to recede and remains under control, and one where a second wave of rapid contagion erupts later in 2020. A single-hit scenario: The current containment measures are assumed to successfully overcome the current outbreak, with the effective reproduction rate declining and staying persistently below unity. Higher hospital capacity and the widespread roll-out of effective testing, tracking and treating are assumed to be sufficient to prevent a resurgence in infections and intensive cases later in the year and until a vaccine becomes available. A double-hit scenario: The current easing of containment measures is assumed to be followed by a second, but less intensive, virus outbreak taking place in October/November. This could be because of seasonal factors in some countries, particularly in the Northern Hemisphere, or because containment, test, tracing and isolating is not as efficient as expected. It could also reflect insufficiently high cumulative infection rates to generate adequate herd immunity, a lack of suitable treatment measures and the unavailability of a vaccine. Further outbreaks in 2021 are assumed to be avoided due to pharmaceutical breakthroughs, but these remain a significant downside risk. Which is more likely – a double or a single? The following chart, from the Financial Times, shows that in many countries COVID-19 infections are still in the first rapid growth phase and not even close to receding. In the case of the USA the number of confirmed cases reached 30,000 in March and then fell to just under 20,000. In the last two weeks, however, it has moved back to over 27,000 and is expected to move higher still as the consequences of easing lockdowns feed through. The UK has managed to get its daily new cases down to 1,200. But that is merely the officially confirmed cases. The reality is that at least three times that number each day in our society catch the disease and potentially pass it on (the average pass on rate is a little below one person passes on to one person). And we hear this morning that Boris Johnson will overrule scientists and open up the economy including 1 metre distancing, opening pubs etc., which means many people will barely social distance (daily new cases in other countries relaxing lockdown: France 483, Germany 575, Italy 204, Spain 573). The greater risk of a resurgence in the UK means I will pay more attention to the OECD’s second wave scenario in what follows. OECD main findings “By the end of 2021, the loss of income [globally] exceeds that of any previous recession over the last 100 years outside wartime, with dire and long-lasting consequences for people, firms and governments.” The consequences of one-seventh of the normal output of UK goods and services not appearing this year are bad enough to bear, but the even worse news is that we don’t get all of that level of activity back for a very long time. The OECD say: "The recovery is likely to be hesitant and could be interrupted by another coronavirus outbreak if targeted containment measures, notably test, track and trace (TTT) programmes, are not put in place or p ………………To read more subscribe to my premium newsletter Deep Value Shares – click here http://newsletters.advfn.com/deepvalueshares/subscribe-1 Ben Inker is GMO’s Head of Asset Allocation (GMO is a $118bn fund). In GMO’s most recent letter he offered some thoughts on the economy and the market. The title puts his argument pithily “Uncertainty has seldom been higher; oddly, neither has the stock market”.

Since March we have had six years of “normal” equity returns in the space of less than two months, “Meanwhile, our estimate of the downside risks to the global economy have not notably lessened.” The GMO team have taken advantage of this contradiction by selling off equities and increasing long/short trades which allow increased exposure to relatively cheap shares but reduce “the portfolio’s sensitivity to overall market direction”. I’m guessing, but I think what that means is that a lot of money is used to gain exposure to the upside of the market, e.g. going long by buying shares in, say Proctor and Gamble. This trade is matched by the same amount of money taking positions shorting a matched company, say Unilever, or shorting the market as a whole, e.g. through derivatives such as options or futures. At the same time a bunch of deep value shares have been bought. Thus, the long/short combination allows them to be sanguine about the market’s movements – if it goes down they gain on the Unilever short say while losing on P&G long position, etc. But being long on value investments allows a good overall return when the neglected, unloved shares out-perform. (I’ve gone someway down this road myself with a combination of put options on the Dow and the holding of value investments reducing my concern about market direction, i.e. I’m OK markets fall because I gain on the put options; and I’m OK if markets rise because I gain on the value shares) Nothing but good news is expected Inker says that the markets seem to be pricing in something close to the best-case scenario. This is possible if a vaccine/treatment is found quickly. But in the absence of that “we believe substantial losses would b………………To read more subscribe to my premium newsletter Deep Value Shares – click here http://newsletters.advfn.com/deepvalueshares/subscribe-1

On Thursday I bought put options on the Dow Jones Industry Average Index. The exercise price is 180 and this right to exercise expires on the third Friday in December. I’ll explain.

Let’s start with what a put option is: a right, but not an obligation, to sell the underlying at a fixed price at some point in the future or over a period of time. Applying that to the Dow: when I bought on Thursday the underlying, i.e. the DJIA stood at 26,000. A put option gives me the right to sell the Dow at a set price in December. A slight complication: instead of the straightforward Dow the DJIA number is divided by 100 for the option contract. Thus if the real Dow is at 26,000 the option that is “at the money” is expressed as 260 (an at the money option has an exercise price the same as the current market price). Each of those points is worth $100. I’ll illustrate with the put that I purchased on Thursday: I bought the right but not the obligation to sell at 180. If I was to go ahead and exercise my right I would be selling 180 x $100 = $18,000. But, with index options I do not have to sell the underlying because these are what is called “cash settled”. That is, only the difference between 180 and the value at expiry is paid over in cash (I don’t sell the 30 different company shares making up the Dow). Obviously, I would not want to exercise the right to sell at 180 when the market is at 260. This means that the option does not have intrinsic value (it is “out of the money”). If I had bought a 270 put option instead I would have the right to sell at 270 x $100 = $27,000. And I could buy that index at 260 x $100 = £26,000 to offset. Overall a profit. This put option has intrinsic value of 10 points or $1,000 (it is “in the money”). But such an option costs a lot more than the heavily out of the money one I did buy. I paid 3.90 points for the right to sell at 180. Those 180 points are worth 180 x $100 = $18,000, whereas my option cost 3.90 x $100 = $390, which is 2% of the underlying. I have between now and the third Friday in December for my option to gain some intrinsic value. It will not do so if the Dow stays above 18,000. So, if the underlying fell to 170 (that is 17,000 on the real Dow) I would have the right to sell at 180 while being able to “buy” at 170. The market organiser (CBOE in Chicago) will cash settle with me for 10 points per contract (180 – 170), each point worth $100, thus sending me $1,000 in December. Thus, I have a highly geared position on the Dow. For a large range of Dow values in December I receive nothing, but when (or, rather, IF) the Dow falls below 18,000 I start to gain quite high percentages. If the Dow falls all the way to 14,000, off about 46% from its current level, then the amount I receive is 9 times the amount I put down as a premium – see table. Real Dow in DecemberDow for the purpose of option pricingI can sell atNumber of points differenceValue of optionPercentage change for the 3.90 points x $100 = $390 paid for each option 26,000260180negativeExpires worthless – all option premium lost-100% 18,0001801800Expires worthless – all option premium lost-100% 17,00017018010 ………………To read more subscribe to my premium newsletter Deep Value Shares – click here http://newsletters.advfn.com/deepvalueshares/subscribe-1 We’ve all heard of Ben Graham’s Mr Market, a fable kept preeminent in Warren Buffett’s mind ever since he learnt it by reading The Intelligent Investor in 1949. Buffett gave a twist to the fable in his Mr Farmer story told at Berkshire Hathaway’s virtual AGM a few days ago.

Buying a small part of a business, not counters in a game of speculation “We’ve always looked at stocks as being part of a business. People bring the attitude toward them too often that, because they are liquid and quoted, that its important to develop an opinion on them minute by minute. That’s really foolish when you think about it. That’s something Graham taught me in 1949: that single thought that stocks were parts of businesses and not just little things that moved around – charts were popular in those days.” Buying a farm with a peculiar neighbour “Imagine that you’d decided to invest money now, and that you bought a farm; say 160 acres at X per acre. And this farmer next to you bought 160 acres of identical quality. And this farmer was a very peculiar character because every day that farmer, with the identical farm, says ‘I’ll sell you my farm, or I’ll buy your farm, at a certain price”, which he would name. Now, that’s a very obliging neighbour. That’s gotta be a plus to have a fellow like that on the next farm.” Shares are different “You don’t get that with farms; you do get it with stocks. If you own 100 shares of General Motors on Monday morning someone will buy your 100 shares or sell you another 100 shares at exactly the same price. And that goes on five days a week.” Intrinsic value “When you bought the farm you looked at what the farm will produce- that is what went through your mind. You say to yourself, I’m paying X dollars per acre and I’ll get so-many bushels of………………To read more subscribe to my premium newsletter Deep Value Shares – click here http://newsletters.advfn.com/deepvalueshares/subscribe-1 |

Glen ArnoldI'm a full-time investor running my portfolio. I invest other people's money into the same shares I hold under the Managed Portfolio Service at Henry Spain. Each of my client's individual accounts is invested in roughly the same proportions as my "Model Portfolio" for which we charge 1.2% + VAT per year. If you would like to join us contact [email protected] investing is about making the right decisions, not many decisions.

Categories

All

Archives

May 2023

|

RSS Feed

RSS Feed