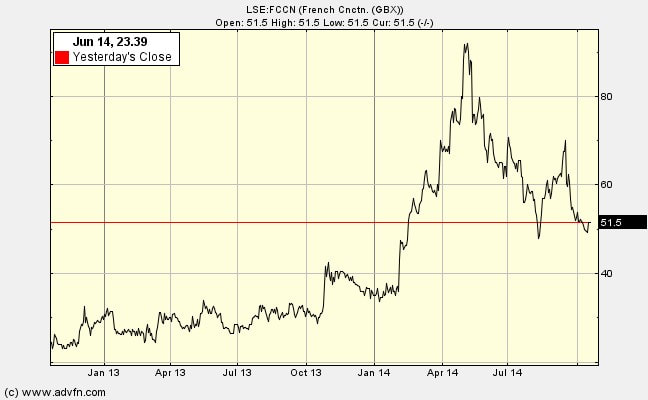

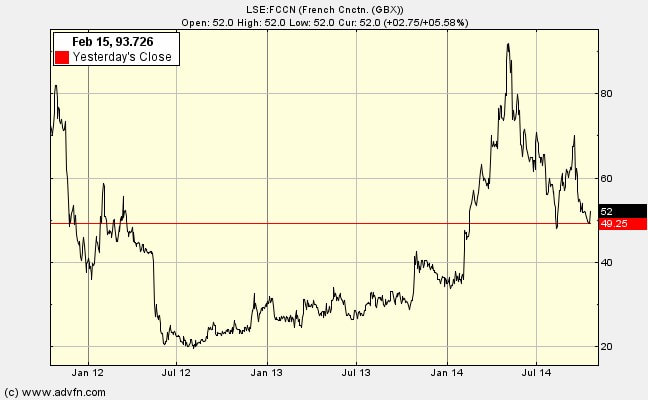

Newsletter 11 - french connection - deciding whether to invest back then 28th october 201422/7/2020 Before I post on whether FC (LSE:FCCN) is a good investment now, I’ll go over the line of logic I was following in July 2013. I mused on the following ideas: "Don’t forget that Graham did not mechanically purchase all NCAV shares. He also examined for business prospects, stability and quality of management. Here we are on shaky ground with FC because we really do not know, we can only think probabilistically  But then, with this investment category we are not doing a Warren Buffett & Charlie Munger ‘Inevitable’ analysis in which we expect excellent management, economic franchise with a deep and dangerous moat and fantastic stability in every case. Graham thought that high NCAV firms might turnaround because of one of the following:

In the case of FC I cannot see clearly the most likely reviving factor. I can say that exit from the industry by rivals is very unlikely to be valuable because there is also so much industry entry to keep pressure up. Liquidation will not release value because everything will be taken by the landlords. The main hope is a change in the quality of management. Are they now properly awake? Is the new talent really good? We will not know for some time – we can only play the odds." UPDATE (OCT 2014): New management seem to be improving matters. In the next blog I provide the data which contributed to the decision to invest in 2013.

1 Comment

Does it make sense to invest in a share that you think has a more than a 50% chance of declining? If you get the answer to this one right you can make a lot of money. I asked this question on the ADVFN bulletin board when I was considering buying French Connection (LSE:FCCN) in July 2013. You might find the answer useful – it’s a simple principle, but one we humans are apt to Forget.

July 2013 post: I have been reading the intelligent debate between PaulyPilot and CR [on ADVFN BB] with great interest. Thank you for bringing such thoughtfulness and expertise to the table. I have an idea that I think may help. As you’ll see I agree with both of you!! First let me start with an analogy: You go to the racecourse with two friends. One friend says that the positive points about a particular horse outweigh the negative, the other says that the negative outweigh the positive. After listening to the debate you think that the chances of the horse being a winner are only 40%. Should you place a bet? Rationally, that depends on the odds you are being offered. If you can get 5 to 1 odds then, even though the pessimistic person is more likely to be right, if you bet on many horses like this then over a period of time you will come out fine. Paul, with a great deal of industry knowledge, says that if the management do get their act together then this can be a multi-bagger. I agree, but that is a big ‘if’. If I do buy now at 30p, then in three years the chances (say 60%) are that I will look back and say that the company fell at a fence and I lost my Money. Does that make it a bad investment decision? No. Benjamin Graham and Warren Buffett tell us that investment is not about getting every decision right in the sense that every one turns out a winner. You must factor in the odds as well. Thus if you purchase 10 shares in this category of Graham’s Net Current Asset Value shares over a period of years you will come out fine. You might like to see the evidence for such an assertion. As well as Graham’s record you might like to look at an academic paper I wrote with Xiao Ying for The Journal of Investing. Being a statistical piece of work we were unable to filter out plain no-hopers or those with hidden liabilities and yet, even with that constraint, the overall portfolio performance was very good over two decades. We have to be prepared to take a chance on an individual share when it forms part of an out-performing portfolio. In the paper we did not manage to include an analysis of the proportion of shares that individually underperform within a high performing portfolio. However, in another paper examining the return reversal method we found that that only 47% of share bought earn positive market-adjusted returns during the five years following portfolio formation. On average, 7% are liquidated during the 5 years, leaving 46% that survive but under-perform the market. Despite this this 'loser' portfolio outperformed the market by 8.9% per year on average. I’m looking for ‘a good business’. And I expect to find it, even for companies on low prices relative to the Net Current Asset Value. This requires investigation and understanding of some vital qualitative elements:

Earnings power One indicator of good prospects is a satisfactory level of current earnings and dividends, and/or a high average earnings power in the past. No projections of great things to come, other than those relying on ‘facts’ proven in the data. And don’t rely on past data alone: it may mislead. Take Tesco, for example, the past ‘facts’ look very strong. But as we all know, the competitive environment can change on the ground. We must scan beyond the data for signs of vulnerability. Earnings power is not the current earnings, but is derived from a combination of actual earnings over a period of years (5-10 years) and estimated future earnings over say five years in the future taking into account the competitive strengths of the business vis-à-vis rivals, suppliers, customers as well as the potential for new rivals to enter the industry and for substitute products/services damaging the firm (e.g. the internet provides a substitute for travel agents, recorded music distribution and book selling). More on competitive position Some industries are structured so that they provide the players within them a high return on capital employed. These firms can sell their products at a high margin over the cost of production. Other industries are notorious for the perpetually poor return on the shareholders’ cash that they use. It seems that they are locked into poor bargain positions with customers and/or suppliers, they have several rivals all clamouring for market share launching into calamitous price wars. Quality of management There are two aspects:

Financial stability You do not want to be in a company with high levels of borrowing or highly variable income flows – steady as she goes is much more relaxing. Industries that are not subject to much change are likely to be stable; so bio-tech and computer game software is out, industries such as selling boring widgets is in (probably). The next blog will apply some of these ideas to French Connection It is not enough simply to buy every company that has a NCAV under current price. We need to be more selective than that. (See blog on 15th October for definition of NCAV). To start with I whittle down the short-list of potential NCAV using a ‘throwing-out’ checklist:

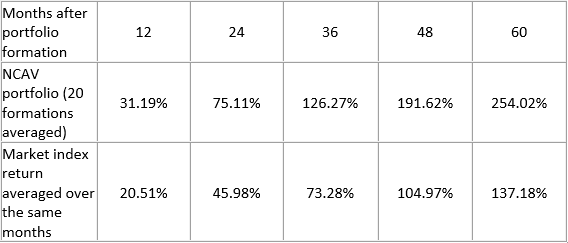

Foreign and opaque For a start, I’m hesitant about investing in companies run from abroad. I don’t have a clue about corporate governance procedures, disclosure requirements, political interference, etc., for companies run out of, say, Russia or China. I’m even reluctant to plump for US companies because I like to be able to judge the sustainability of the business and the quality of the management. How can I do that when I’m thousands of miles away, ignorant of the market environment and unable to meet the managers. At least with French Connection (LSE:FCCN) I can see what they are doing on the high street, I have some grasp of retailing in the UK, etc. Cash shells I’ve also rejected companies for further consideration because they seem nothing more than cash shells with thin management and even thinner business legs. Natural resources Then there are the mining (and oil) companies. Mark Twain said that mine is a hole in the ground owned by a liar. I would not go so far as to say that they are run by liars, but just what are those holes worth? Such imprecision makes me nervous. Managers/controllers looking after number one On examining accounts and reading between the lines I suspect some managers are syphoning value from the company. I spotted one team who set up a separate company with 50% of its shares owned by them. This unquoted company was then given control over various assets of the quoted company. Then there are those which seem to have a history of playing games with the accounts. You cannot make a good deal with a bad person. One family-dominated company I examined issued options allowing the family to buy shares amounting to more than the market capitalisation. You need to dig deep to find these little facts. I would rather invest in a traditional manufacturing or service business, with long-standing experienced executives, than one run by sharp City-types who dart in and out of companies playing financial manipulation games. Avoid those that appear to be the playthings of the main shareholders who show little awareness of their responsibility to minority shareholders Hidden liabilities Watch out for the hidden liabilities that wipe out NCAV, e.g. large pension deficit. Having listed what I’m looking to avoid in this blog, the next will outline the key elements I’m looking for in terms of prospects for the business. Newsletter 7 - Proof that net current asset value investing gives great returns 21st october 201421/7/2020 I’ve made you wait long enough - I’ll now explain the results of the research for a twenty year period employing the Net Current Asset Value approach for London shares. As a Professor it was my job to supervise PhD students and publish original research. One of the most interesting studies asked the question: “If, over the period 1981 to 2000, you had bought a series of portfolios of shares whose prices are less than two-thirds the Net Current Asset Value (see blog on 15th October for definition) would you have outperformed the market?” We (Ying Xiao and I) imagined that we had gone back in time. We searched the entire Official List each July (average of 1,109 companies). If the ratio of NCAV to market capitalisation is greater than 1.5 we imagined buying. We then ‘held’ the portfolios for five years, noting the month-by-month performance and compared it with the general market. The average number of companies fulfilling the criteria was 23. The average performance of the 20 portfolios is striking: In the first year after portfolio formation the NCAV shares averaged a return of 31% which was almost 11% more than the market. And it just got better and better the longer you held the shares (up to five years). This is good news for those of us looking to reduce transaction costs and delay tax payments on gains – just hold onto the shares. After 5 years, on average, NCAV ‘investors’ had turned £10,000 to £35,402. Average raw buy-and-hold returns  There are many other tests in the paper, e.g. the NCAV are shown as less likely to be liquidated than the average share – over 5 years the liquidation rate is 2.6% compared with 4.2%. I guess all those BS assets must be good for something. For more detail you can read an earlier draft of the paper on my personal website: www.glen-arnold-investments.co.uk.

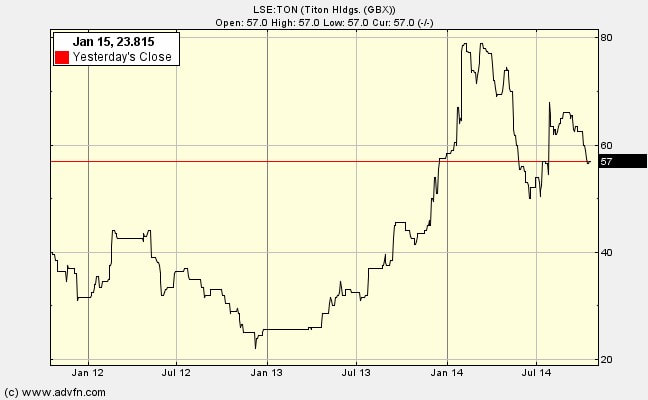

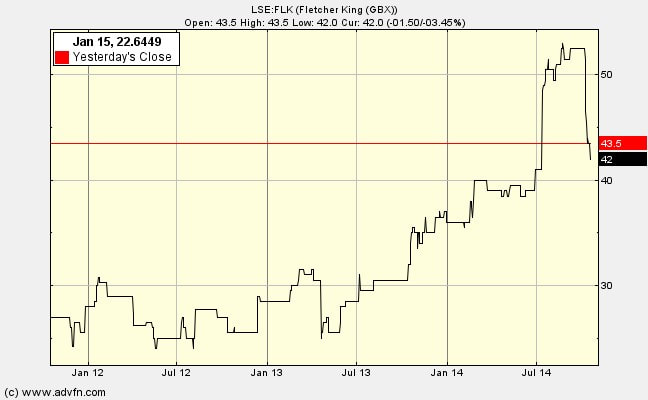

Note this paper used a purely quantitative criterion for qualification for inclusion in the NCAV portfolios – only whether the share price is one-third or more below the NCAV. In an academic paper we cannot test subject factors such as ‘prospects for the industry’ or ‘quality of management’ because these factors though vital, are subjective. Thus we can improve the sophistication and outcomes by overlaying the mechanical NCAV criterion with judgment concerning the quality of the business – see next blog Newsletter 6 - Why should a share with high Net Current Asset Value rise? 20th october 201420/7/2020 Companies going through a torrid time, a few years of loss-making, or suffering from an economic or industry decline, are usually subject to a great deal of market pessimism. Sometimes this is indiscriminate. Alongside the dumping of dross, there is dumping of sound companies, where there are good grounds for believing that recovery will eventually occur. There are four possible paths of development that might reverse the destruction of value through the gradual dissipation of assets: First: Earning power can lifted through an improvement in the economic background. This might be the result of a general economic recovery. A good example here is Titon, (LSE:TON), a supplier to the house-building trade (window parts and whole house ventilation). The potential for a bounce-back in housing in the UK and Korea was not factored into the share price when I bought in 2013 – see my blog on 13.10.14 for the performance numbers – up 69%. I’ll explain my rational for investing in Titon in another blog.  Sometimes the low share price seems very strange. In the case of Fletcher King, (LSE:FLK) a commercial property servicing company, (up 50% since I bought in August 2013), the market seemed to ignore the steady profits year-after-year through the recession, and its high operational gearing in the five years to early 2013. The market seemed to focus on the despised sector it was in. When there was a 20% rise in turnover in 2014 profit doubled and the share rose. Now that economic growth has resumed, the company is in investor's sights again.  Earning power can also be lifted through the effects of ‘exit’ from the industry; competitors go to the wall or withdraw from some activities, allowing the few left standing to increase prices and raise profits; the share price rockets. Second: Management stir themselves. They may be competent, but faced a fierce onslaught. Perhaps they will regroup, learn from past mistakes and attack with renewed vigour. Alternatively, less able managers are replaced with more able. This happened with French Connection (LSE:FCCN) – up 62% over the 14 months I've held it. The clothing offered is now more attractive, unprofitable shops are being closed, etc.  Third: A sale of the company to another.

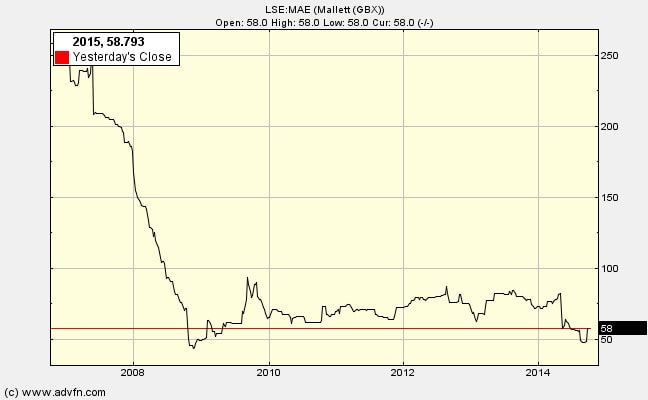

The buyer should be willing to pay the liquidating value at least and so the NCAV investor gets a boost (this is a moot point for Mallett, arguable sold cheap). Fourth: Complete or partly liquidation. The management of a corporation selling at less than the liquidating value must provide a frank justification to shareholders for continuing. But, it is very difficult to get some of these turkeys to vote for Christmas! As I found with Mallett. I like it when the stock market plunges. I know it sounds perverse for someone with a substantial equity portfolio. Don’t I know that the value of my portfolio has just gone down??

Well, actually, the value may or may not have gone down. What has gone down is the market price – a totally different thing to value. Remember, we are investors not speculators. As investors we look not to short-term market movements to make money by timing our purchases just before the market rises and sales just before it falls, but as investors we buy portions of a business, a business that we have some understanding of, a business we have analysed. If that business becomes cheaper to buy, should we be upset? The price of burgers Try this analogy: You expect to be a consumer of food for the next decade, right? Would you prefer if, over time, food prices rose or fell? Of course, you would like prices to fall so that you can get more for your pound. Now another analogy, closer to stock market investing: You have a portfolio of corner shops built up by buying every three months. In each case you did a thorough analysis before buying and subsequently. Logically, you will have estimated of the prospective future cash flows flowing to you; and compared this with your required rate of return on the money you invest. Now imagine the price of corner shops plunges for reasons unconnected with the corner shop business (fears over Chinese shadow banking blow-up, commodities down, US shares down, European stagnation, Ukraine, Ebola). Are you upset about your portfolio? – only if you planned to sell in the next few months. So, no then. Will it stop you buying more shops? – no, they are now cheaper, you can buy more for your pound. The rational investor Investors judge value based on the expected cash flow to be received from the asset whether that is corner shops or 1000 shares in BP. They do not judge value by what Mr Market is currently offering to buy or sell at. Mr Market is sometimes overly exuberant given the underlying value and sometimes he is over-pessimistic. Are you to judge the value of your assets by Mr Market’s manic-depressive leanings? Market prices are useful to us, not as guides to value, but as opportunities for us to exploit. We buy when there is a large margin of safety between our assessment of value and the market price being offered. If there is no large margin available then stay in cash. When the market goes down there is more chance of a margin of safety being created. Preparation……..discipline……patience….and only then….decisiveness I keep a watch-list of companies currently too expensive relative to fundamental value. When the price falls to my target range I get excited – falling prices are wonderful. We have usually made our best purchases when apprehensions about some macro event were at a peak. Fear is the foe of faddist, but the friend of the fundamentalist (Warren Buffett, 1994) Determine value apart from price….progress apart from activity….wealth apart from size. Warren Buffett Be fearful when others are greedy, and be greedy when others are fearful. Warren Buffett, 2008 In previously blogs I described the extraordinary returns available to Net Current Asset Value, NCAV, investors. Before I present some academic evidence of success over a twenty year period I would like to share with you some thoughts on what pushes these shares down in the first place, and what might cause them to rise. Going down…… There are three reasons that even companies with large surpluses of current assets over liabilities fall in market price to below NCAV: First: The managers pursue value-destroying activities that whittle away shareholder’s assets though losses year after year. Second: The stock market has, in its manic-depressive fashion irrationally pushed shares down to unreasonable levels. This is particularly the case for smaller firms which can be badly neglected by the investing institutions. I have worked for a fund management house with a rule that no company with a market capitalisation under £200m is to be looked at. They need to buy shares in volume, and to be able to get out in volume. Thus many companies have no professional analysts examining their prospects and precious little institutional money flowing into their shares. This presents excellent opportunities for the switched-on small investor looking to invest a few thousand pounds. Third: Shareholders have not pressed the company to do the right thing by shareholders. This was brought home to me this summer when I attended the AGM of Mallett (LSE:MAE), the antiques dealer in Mayfair. As far as I could tell, after five years of losses the operating business was appalling and should either be greatly reduced in size to release money to send to shareholders, or if things continued to deteriorate, all assets should be liquidated and the money handed back to shareholders – more would be generated that way than the current market capitalisation.  To give some idea of the calibre of the directors: the CEO did not attend his own AGM – busy in Asia, apparently. Needless to say, throughout the years of loss making the BoD had paid themselves very handsomely.

Clearly, the shareholders needed to act to stop the continued diminishing of shareholder value, and yet only two shareholders attended the AGM – it was not even that good, as the second attendee was a ‘representative’ of the Weinstock family, long-term 30% shareholders. Making my points about boardroom pay, long- term losses and the need to consider liquidation, I did not receive any support from other shareholders – they were a bit scarce at the AGM, and had not responded to my calls on the ADVFN bulletin board. So, management continued on its merry way, lowering shareholder value with every step. We have been saved, if you can call it that, by Stanley Gibbons offering to buy the company for 60p per share. It just shows you that (a) management teams can keep on destroying value for a long period before shareholders stand up and demand reform, and (b) you have to be sceptical in accepting BS numbers - Stanley Gibbons are buying at a one-third discount to reported NCAV. Oh dear, I have run out of space to present the ideas on what might correct the downward movement in share price. Sorry. I’ll do this in the next blog. newsletter 3 - Companies selling for less than net current asset value 15th of october 201416/7/2020 Price is what you pay, value is what you get. Believe it or not, hidden in the depths of the stock market can be companies that are selling for less than the value of their current assets.

More remarkable still is the fact that if you deduct all liabilities, both long- and short-term, from these current assets you can still find some companies are selling for less than this net current asset value. This is even more astonishing if we consider that we have completely ignored the value of the long-term assets (non-current or fixed assets). They are valued at zero in this approach. This is conservative valuation taken to an extreme. It may be that the long-term assets comprise of buildings, vehicles, plant, etc., with a significant market value and yet we ignore all of that – we count it at zilch. Two more layers of caution So in Net Current Asset Value, NCAV, we take current asset values only and deduct all liabilities. But before we compare that with the market price there are yet another two layers of conservatism. First We do not take the current assets valuation number in the balance sheet at face value. It could be that you want to build in a margin of safety on the inventory valuation. Perhaps you want to allow for managers being too optimistic in their estimation of what they can sell partly-made or finished goods for. Perhaps you only value it at 66% of the BS value. Similarly with receivables (‘debtors’ in old money); the managers may be more optimistic than you in guessing the proportion of customers who will not pay. Perhaps the receivables figure should be lowered by 20%. Second We must ensure that the qualitative characteristics of the company are sound. This falls under three categories (1) Prospects for the business, (2) Quality of management, (3) Financial stability. These will be looked at in a future blog. The next blog considers what leads to such lowly priced shares. After that I describe what might cause these highly neglected companies to generate high returns for shareholders in the future. After all, they have usually displayed large share price falls in the recent past and are often unprofitable The last blog showed how my 2013 portfolio based on Benjamin Graham’s Net Current Asset Value approach has worked – up 40% in a year (in a flat stock market). I explain more about the technique here.

As a young man Benjamin Graham was a successful fund manager in the 1920s. Then the Wall Street Crash happened. In the years that followed he thought about the difference between investment and speculation. One of the factors is that speculators often put a great value on hope. They forecast a bright and glorious future regardless of the absence of solid ‘facts’ from the past or the present to support that hope. He learned the hard way to consider the what-if questions, e.g. What-if the economy suddenly stops growing? What if there is a changed consumer mind-set resulting in much lower sales of the firm’s product? What if the assets in the balance sheet can’t be sold at that valuation? Bridge building and the investor His cautious attitude is encapsulated in the guiding principle followed by engineers when designing a bridge. They do not just build-in strengths to withstand all normal stresses and strains. They build-in a large margin of safety, so that if unusual winds or loads impact it the bridge will still stand. So it should be with investors. They must allow a large margin of safety. Given the ‘facts’ available, that is, trustworthy balance sheet net assets and proven earnings, will this company be able to withstand shocks. Furthermore, is the current price placed on the company by the market significantly below the value that you would place on it if you were buying it as your family business in a private transaction, given very realistic assumptions about the assets, liabilities and earnings power? Buy at bargain prices With this mind-set Graham set to work looking for companies significantly under-priced. Between the mid-1930s and mid-1950s his main approach was to buy when the market was selling at less than the net current assets. He found dozens, sometimes over 100, in the Depression. Companies were selling at less than the realistic liquidation value of the balance sheet. Over those 20 years he significantly out-performed the market. Some of these companies were selling at less than the cash on their balance sheet. In case you were wondering if this phenomena disappeared after the extraordinary circumstances of the 1930s, think again. Many hi-tech companies of recent times raised large amounts of money, then the stock market crashed, they fell out of favour and market capitalisation fell below BS cash. There is much more to Benjamin Graham’s approach than this. The next blog will detail the quantitative rules. |

Archive

I wrote newsletters for almost 10 years (2014 - 23) for publication on ADVFN. Here you can find old newsletters in full. I discussed investment decisions, basics of value investing and the strategies of legendary investors. Archives

October 2020

Categories |

RSS Feed

RSS Feed