|

I thought I’d start off the blog by posting key things investors must remember to help stay on the narrow path. Here are my initial thoughts on the top ten. Perhaps we can add to the list – what do you think?

1. If you do not understand do not buy it. View shares as part ownership of a business, not as gambling counters in a game of chance. Be a business analyst trying to understand what makes it tick, rather than a share analyst. 2. The thoughtful, dedicated private investor can out-perform the professional They have many advantages, including concentrating a portfolio on the few best investment ideas, taking the risk of being different from the herd, and finding good companies in everyday experiences. 3. The market is there to serve you not to guide you Many treat market prices as a guide to the value of a share. The market, in its manic depressive fashion, often sets prices that are far from the true value of the business. Be independent, evaluate firms and exploit market prices rather than be led by them. 4. Invest don’t speculate An investor thoroughly analyses to understand the business, only buys when reassured on the safety of the principal and aims for a satisfactory return, rather than over-reaching for extraordinary returns. Operations not meeting these requirements are speculative. Speculators focus on guessing short-term price moves. They do not thoroughly analyse a company, do not factor in a margin of safety and do not look merely for a satisfactory return, but stretch the risk boundaries in targeting extraordinary returns. Speculators actually think they can spot the bottoms and tops, and buy or sell appropriately. The great investors state that after decades of experience that they do not have a clue where the market is headed over the next 6-12 months, yet punters with one-hundredth of their experience think they can do it! Share prices have a strange psychological effect on the speculator: they demand more when the price has risen and demand less when the price has fallen. 5. Don’t pay high fees Fund managers can take away the bulk of the investment gain. Fees of 1.5% sound low, but can remove one-third of your gain. A fund manager charging 1.5% p.a. better pack some real dynamite, when ETFs charge only 0.3% and you have the option of creating your own portfolio with no management charge 6. Margin of safety When valuing shares expect to arrive at a range of reasonable intrinsic values rather than a single point. If that range is £2 to £3 do not buy if the current price is £1.95 - that is not a big enough margin of safety to allow for analytical errors or business vicissitudes. 7. Diversify, but not to mediocrity You are vulnerable if you invest in only one share, so diversify. Beyond 10 the benefits of further diversification become small. Better to concentrate your knowledge and hone your analytical edge. Stay within your circle of competence. 8. Stock market mispricing knowledge Become aware of the remarkable findings in academic papers on whether the stock market can be beaten. On the whole they find that it is very difficult to outsmart the markets (that is, performing better than just buying a broad spread of investments and going to sleep for a decade or two). However, there are some nuggets of gold hidden in the academic jargon and maze of statistics. The findings provide rigorously-derived corroborative evidence of what many great investors have been telling us for decades, and, in some cases, take things a little further. 9. Read the philosophies of the great investors Learn from their hard earned experience of what works and what does not. Learn from their mistakes – you can’t live long enough to make them all yourself. 10. Enjoy the journey as well as the proceeds, because the journey is where you live. Enjoy your investing. If you don’t enjoy it then hire someone else to do it for you (if charges are reasonable).

0 Comments

Sit on your ass investing. You’re paying less to brokers, you’re listening to less nonsense, and if it works, the tax system gives you and extra one, two, or three percentage points per annum. Munger

It takes character to sit there with all that cash and do nothing. I didn’t get to where I am by going after mediocre opportunities. Munger Your goal as an investor should simply be to purchase, at a rational price, a part interest in an easily-understandable business whose earnings are virtually certain to be materially higher 5, 10 or 20 years from now. WB (BH 1996) I fear that these directors are not improving in the way I set out in my Autumn justification for investing: indecision on New York space, indecision on Finance Director layoff, not selling stuff effectively, apparently the Internet is this revolutionary new tool for selling antiques..umm

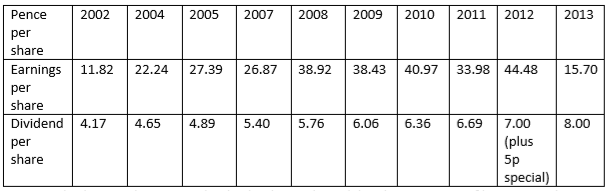

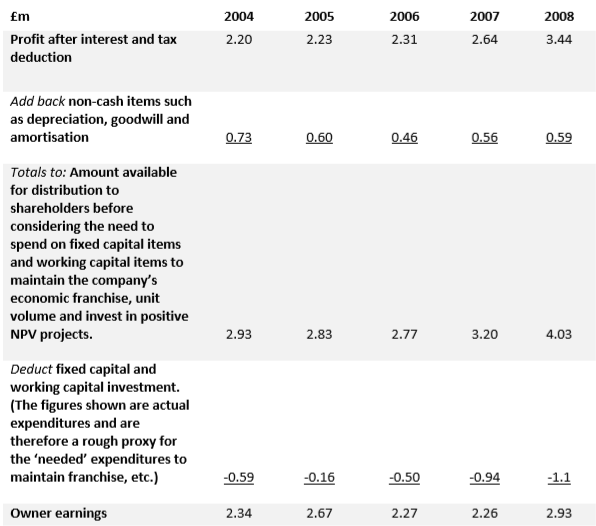

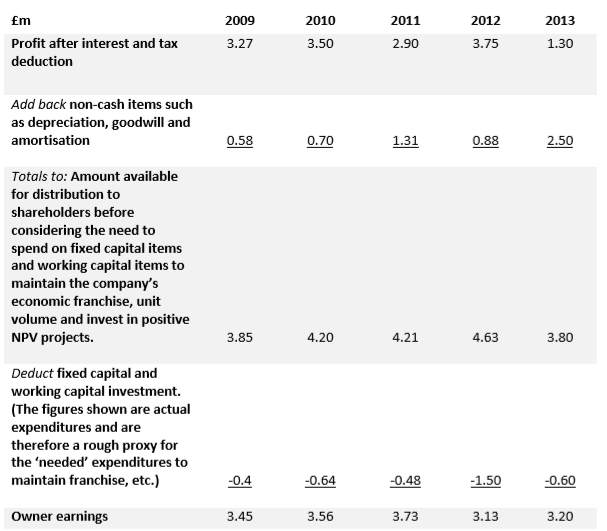

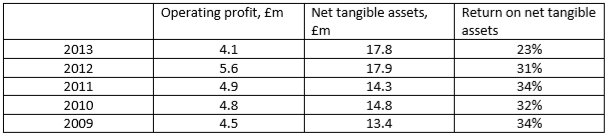

These are the questions I intend to ask at the AGM meeting. First. When the special dividend has been paid shareholders will be holding net assets of around £12m to £13m. It is reasonable for equity providers of capital to a business to expect to receive a minimum return of 8%. That would mean Mallett should be, consistently, year-after year, producing at least £1m profit after tax. If there is no reasonable prospect of this then the logical course of action is to return shareholders' money to them. Imagine if 5 years ago that you (addressed to directors) were persuaded by a friend to invest £15m in the equity of his business. The friend has run the business in such a way that losses were made each year. Now there is £12m of your money left in the firm. Your friend wants to carry on the business that he loves (surrounded by beautiful things, nice salary, trips abroad, etc) When you first invested you said you needed at least an 8% p.a. return. It seems that your friend is incapable of generating even £1m per year on the money you have entrusted to him. So what will you say to your friend? Carry on? or, I want my money back so that I can invest it in other businesses that do produce a decent return? I did consider using Jesus' parable of the talents, but even the worse character there returned the talent. So my questions: 1. Why should we not liquidate the assets of the company to release shareholders money? 2. Why do you not examine each section of the business in terms of (a) how much of shareholders money is devoted to this activity, and (b) are we generating a large enough ROCE? and (c) should we cut value-destroying activities? 3. Do you agree with this idea: By all means pay the current remuneration to directors if they achieve the £1m profit after tax target. But until they do this Board remuneration should be no more than £40,000 per person? Second: Can I direct your attention to Note 18 in the accounts 'Receivables'. I'm afraid I do not understand - can you help me please? First, why do wealthy customers buying antiques need to be offered credit? Also, why, when gross margins are so small, do you even contemplate giving credit? Why is it that such a high proportion of customers do not pay on the due date? £637,000 is outstanding 6 months after 'sale'. What is going on? Do the shareholders as a body need to get the fraud police involved? Are shareholders assets being misused in any way? Can we hold the directors to account if the receivables figure at next year-end is not close to zero? A report on the AGM: The first interesting fact is that the CEO had better things to do – he was busy selling antiques in Hong Kong. Only three directors attended – the two NED and the FD. At first I was shocked at this contempt for shareholders then I looked around the room. I was the only shareholder present (I think this is the case: there was a young lady, but I think she was with the company and did not ask any questions). My eldest son accompanied me, and there was a young gentleman who was a ‘representative’ from the Weinstock Trust (he did not ask questions either). So, how can you expect directors to take their shareholders seriously if shareholders do not show an interest in their company by turning up once a year to the AGM – a self-reinforcing cycle of depressing misunderstanding and suspicion? Directors’ answers to my questions: To liquidate the assets in a ‘fire-sale’ (who said anything about a fire-sale) would result in NAV being below the current share price. They are optimistic (but not so that they will part with their money to buy shares) that the company is on the mend: new sale opportunities in Middle East, Asia and South America; economic recovery; the website and Masterpiece. ‘Analysts’ are now forecasting profit for 2014 of £400,000 and for 2015 £1m. Therefore we are getting close to my target profit numbers - supposedly. Are they willing to put their money where their mouths are? Well, you see, if you reduce the remuneration of the senior team they will walk – already a New York expert has crossed over to Sothebys. I understand that argument, if it was imposed. I was looking more for the actions of a decent man to stand up and say that ‘I’m so confident in the turnaround of the company and I feel a sense of moral obligation to shareholders that I will only take a high salary when the shareholders are getting a good return’ I was looking for volunteers with integrity. Blank stares of incomprehension all round. Apparently, many long hours have been spent in looking at individual parts of the business to see where profits can be generated, but I’m not sure that they fully understood the value-based management concept of value generation above the equity cost of capital. My son (a first class business graduate and an entrepreneur) tried in vain to contrast the £11m tied up in fully owned antiques producing very little profit with the near zero company capital tied up in the £20m of consignment stock producing, as a percentage of capital allocated, a nice contribution. They came half way by acknowledging the importance of consignment, and we came half way in accepting that 100% consignment would be a mistake because you must have the freedom to correct the mixture displayed in the show room. Charles, however, could not see why they could not reduce ownedinventory to say £5m (increasing consignment to £30 or £40m) releasing a large sum of money to be paid in a special dividend. One point of optimism: the consignment business will sit nicely with the internet strategy. Charles also thought that the business model of the antiques game was “c**p”. The way it works is that rich bods come along and say I’d like to buy that item at £50,000, put it on my account please. They might pay you 30 days later or 150 days later. You, as the seller, do not know when you will get the money. We were told that the Mallett staff know all these rich bods and that they have only had one bad debt. But, in normal business terms, it is appalling to combine these three things: (1) Gross margins barely in double figures (2) Stock turn of once per year, and (3) Giving generous credit terms. The directors say that they are very frustrated by the credit terms convention enduring in the industry, but that they cannot do anything about it. If they tried to get tough (what I would call normal) then customers will say ‘I’ll go to Sothebys then, who will give me credit’. I wonder, I wonder – I know some very bright 20-somethings who might look at that afresh and find a way of persuading rich bods to pay up. They would probably also shift the business to being very capital-light (special dividends) with Mallett trading on its name as a market-place, as an endorser of quality and as an exhibitor. It would be fun to try (but you would need to retain the goodwill of the antique ‘experts’). I was suspicious of Gurr Johns (Note 29 in accounts) but was reassured that antiques flow through this agent with client contacts – lots of buying and selling, helping both firms. I’ll take that on trust. The voting was interesting. On many issues (including the re-election of the Chairman) around 40% of the votes were against (apparently, Peter G opposed). They looked nervous and I was under the impression that they had received many messages that they are in the last chance saloon. Time will tell whether they really do understand the concept of value creation from the capital you have under your command. It speak volumes to me that the Board members do not buy shares in this company. For now I will hold onto my shares. It’ll be interesting to see how the story unfolds. What larks, eh Pip. Dewhurst is a stalwart manufacturing company run by the same family for a century. It designs and manufactures components for lifts, ATM and other keypads and for trains. The two brothers currently in charge have decades of experience in this field and are supported by a stable professional team. They have grown profits both by organic means with an almost obsessive interest in design prowess and manufacturing efficiency, and by a measured acquisition strategy of companies supplying (generally) complementary products. Often these acquirees have had a long association with Dewhurst as suppliers or customers. Dewhurst are niche engineers, leaders in a number of small fields. For example, they control 90% of the UK market for lift components. The family has stuck to its knitting. Demand for individual product lines can be somewhat volatile from year to year, but because they apply their core knowledge and other strengths to selling into three distinct markets (lifts, trains, keypads for ATMs petrol pumps and ticket machines) and do so all over the world, the various ups and downs generally even out to produce a history of remarkably steady progress. They display resilience through economic vissitudes. There are 3.3m Ordinary shares carry voting rights and 5.2m Non-voting ‘A’ shares. Thus any overall earnings or valuation figure should be divided by 8.5m shares to derive per-share numbers. The Ordinary shares and the ‘A’ non-voting ordinary shares rank equally in all respects pari passu except that the ‘A’ non-voting ordinary shares do not carry the right to receive notices, attend or vote at meetings of the company. Until September 2012 the ‘A’ and the Ordinary shares were priced in the secondary market very close to each other. Then something strange happened given that the economic rights are equal – the voting shares rose a great deal more than the non-voting. Thus today the voting shares trade at £5.20 whereas the ‘A’ shares trade at £3.20. Market capitalisation: 3.3m Ordinary shares x £5.20 = £17.16m 5.2m Non-voting ‘A’ shares x £3.20 = £16.64m £33.80m Revenue split (2013) Lifts £34m Transport £3m Keypads £10m Conventional earnings per shares and dividends per share analysis. In 31 out of the last 32 years the dividend has grown by 5% or more.  Estimated value per share using the dividend growth model and assuming an 8% pa required return with 5% pa future growth in dividend: Price = 8p ÷ (0.08 – 0.05) = 267p Note the very large dividend cover ratio. This might indicate that dividend could be raised significantly if the company does not have good internal projects to invest into. Price-earnings ratio for ‘A’ shares using average eps for 5 years: 320p ÷ 34.71p = 9.2 Owner earnings analysis   To estimate intrinsic value we could take a rough average of recent owner earnings numbers and assume either (a) that this will continue year after year with no growth, or (b) less conservatively, that the annual owner earnings number will grow by, say, 5% per year. Let us take £3.3m as the proven annual earnings power. (a) Assume no growth and a required rate of return on equity of this risk class at 8% per annum: Intrinsic value = £3.3m ÷ 0.08 = £41.25m The company has 8.5 million shares in issue therefore the value of each share (ignoring the premium for voting rights) is £41.25m ÷ 8.5m = £4.85. (b) Assume owner earnings growth of 5% pa. Intrinsic value = £3.3m ÷ (0.08 – 0.05) = £110m On a per share basis: £110m ÷ 8.5m = £12.94 Return on tangible assets employed  With the company displaying a long history of high retaining earnings (low dividend payout ratio) put to good use in acquisitions and organic growth, generating returns on tangible assets of over 30%, there should be significant future growth in owner earnings to look forward to if this performance continues.

Balance sheet strength Net asset value in total; £21.87m Net asset value per ‘A’ non-voting share: £2.57 Net tangible asset value in total: £17.86m Net tangible asset value per ‘A’ non-voting share: £2.10 Borrowing: zero Cash: £10.5m Pension deficit: £10.5m Character of the managers They have stuck to engineering, and with the exception of the mistake of the traffic management business (road bollards), they have focused exclusively on those areas where they have competitive advantage: lift components, keypads, train buttons, etc. However, they are now moving a little further away from the core by going for lift car manufacture and escalator belts. These moves are measured (£1m to £2m purchases every one or two years) and they are still reasonably well related to the core. They tell it like it is. No embellishment, frequently subsequent events show them to have been overly pessimista. Smart in assessing value in forms other than in engineering. For example, they recognised that the value of the factory in Hounslow would be worth considerably more if they obtained planning permission to build houses and then sold the land. It was sold for £6m in cash (£5m plus £1m of VAT) and then they paid a special dividend. The family own over 50% of the voting shares and have consistently demonstrated that they run the business as ‘if they are the sole asset of their families and will remain so for the next century’ (Buffett 1999), with steady growth within their circle of competence, constant bearing down on costs, high quality interaction with long-term customers, conservative investment and borrowing policies. Bulletin Board comments on the character of the managers are overwhelmingly positive. They are highly respected with long track record of treating shareholders well. They have carefully nurtured a family business in which they take great pride. Richard Dewhurst (Chairman) has an engineering degree and an accounting qualification. He has worked at Ford and as a management consultant. David Dewhurst, MD, has an engineering degree and previously worked at a brand design consultancy. Total director emoluments in 2013 were £654,000, with the highest paid director receiving £189,000. Richard Dewhurst bought 2,000 Non-voters in October 2013 at £2.849 Industry analysis (Asking if this industry is likely to achieve high rates of return on capital employed) It is very difficult to obtain information on these niche areas of engineering. In fact I could not find another push button manufacturer – this is more likely due to my unwillingness to search every international market rather than a complete absence of rivals. Much of what follows must be tentative given the poverty of solid data. -Threat of entry to the industry? The costs of entry are relatively low in terms of factory setup costs. However, the extant players have some name recognition and relationships with architects, building constructors and owners. However, in the face of a sustained onslaught from a new entrant offering lower prices this may be a relatively weak barrier. There is some degree of differentiation through design excellence but this is not a very strong barrier. Experience and knowledge of the industry may provide some protection, but it is not insuperable. -Rivalry in the industry? The high margins and return on assets indicate that the industry has settled down to a stable, gentlemanly way of pricing. The size of customer market is growing (more lifts in high-rise buildings, more trains, etc.) and therefore the stress of increased competitive pressure that comes from a decline industry is not a concern. -Substitute products? It is difficult to imagine potential substitutes being created to take away this industry. -Buyer power strength? There are a limited number of lift and train manufacturers in the world. However, these products are not commoditised because of the high design content. They are often specified by architects, e.g. push buttons in the Shard (Dewhurst’s specified). Also, they are not a large proportion of the cost of a lift/train/ATM installation and therefore the buyers may not push too hard on price. The consequences and risks of product failure are high, which also suggests that customers will pay up for quality (or perceived quality). Is it possible that lift/train/ATM manufacturers could integrate backwards and start manufacturing these components themselves thus limiting the prices charged as bought-in items? -Supplier power? Bought-in elements tend to be highly commoditised; many potential suppliers, thus little supplier power. -Industry evolution? Constant technological change is to be expected. This assists the existing highly experienced players so long as they continue to innovate (e.g. adopt touch screen technology – which Dewhurst is doing). Increased urbanisation and high-rise living and working are to be expected. There are 5 million lifts in Europe (278,000 in UK) half of which are more than 20 years old, therefore need replacement/updating to meet modern safety standards. China has 2.2 million lifts, N America 1.2 m and India 0.27 million. Accessibility for disabled is becoming increasingly important, thus more lifts will be needed both in public buildings and in homes. Extraordinary resources Dewhurst might possess, potentially lifting its return on capital employed above the industry average? -Tangible? None -Relationship? Mostly ordinary resources. However, they offer bespoke solutions to unusual requests from customers, architects, etc. There is a strong emphasis on service and quality. -Reputation? Mostly ordinary resources. However, it has been said that ‘Dewhurst’ are synonymous with lift components in the minds of many architects. -Attitude? A possible extraordinary resource. They appear incredibly focused on their niches with a determination to be the best. -Capabilities? The combinations of skills need to supply solutions for clients may amount to an extraordinary resource. This may be based on path dependency, i.e. the route they took, over a century, to get to where they are today, building up skills within the team (and name recognition over decades) may have created competitive advantages. -Knowledge? A possible extraordinary resource. The implicit knowledge of customers, design and technology built over time may allow superior returns relative to less knowledgeable competitors. Are these possible extraordinary resources demanded, scarce and appropriable? -Demanded? Yes, customers do need these technical, design, service and efficiency qualities. They need good relationships with a supplier of specialised components. They need superior capabilities and knowledge of these niche products. -Scarce? I cannot find alternative suppliers. That is my failing I suspect, rather than an absence of strong competitors. However the returns on assets over the past five years indicates that there is not an abundance of similar companies that customers can turn to. -Appropriable? Will the value created by the firm’s output accrue to Dewhurst or be appropriated by employees, suppliers, customers or others? The suppliers of inputs, including employees, seem to have little bargaining strength and so are unlikely to appropriate a high proportion of the value (e.g. no ‘star’ employees on large bonuses). Customers have greater bargaining strength, but Dewhurst’s history of high return on assets indicates that Dewhurst appropriates a great deal of the value they create as well as creating large consumer surplus for customers. Can Dewhurst resources be leveraged? Yes. They are already applying their reputation, contacts, knowledge of continuous improvement in manufacturing, knowledge of customer requirements to the new businesses they acquire in closely-related niches. They can continue to employ these competitive strengths to additional acquisitions. The directors point to synergies in product development carried out in London having an impact on operations in America, Australasia and Asia. Some questions 1. The large decrease in reported profit for 2013 is a concern. Is it a one-off or will the company continue to suffer? Note that operating profit declined by a more modest 27% and revenue by 15%. The largest contributors to the reported profit decline were a goodwill write-off and a return to more normal keypad sales. 2. Will one of the giant engineer companies invade their markets? 3. Will they acquire more companies beyond their circle of competence or that are in industries with poor economic characteristics, as they did with Traffic Management Products? 4. There are a small number of lift manufacturers. Could they gang-up to oppress suppliers such as Dewhurst? They have a history of getting into trouble with the antitrust authorities, e.g. fined €1bn by EC for illegal price agreements in 2000. In 2014 Spain fined four lift companies for trying to keep rivals out of maintenance market. 5. I have not done enough digging yet to be fully confident in my industry analysis and competitive resource analysis. What have I missed? Who are their competitors? The share price of PV Crystalox has declined from 150p in 2009 to 27p, with market capitalisation now at £41m. It also scores highly on Piotroski factos.

It supplies silicon wafers to photo-voltaic (PV) cell manufacturers, most of which are in Asia. A torrid time was had by anyone connected with the PV industry over the past five years as Chinese manufacturers reduced selling prices below cost. Prices collapsed and many companies went bust. Trade barriers were erected in three continents as accusations of dumping flew. PV Crystalox found itself with long term fixed-price contracts to take delivery of silicon. It also had fixed-price contracts with many customers, but the severe decline in product prices in an industry with vast over capacity meant that they could not pay, and so renegotiation and greater flexibility from PV Crystalox was called for. Years of losses and balance sheet write-offs followed. 2012 and 2013 were years of reducing capacity and ‘operating in cash conservation mode’. Whereas shipments in 2011 were 384MW, they were 108MW in 2012. They rose to 211 MW, but this is largely due to selling off excess inventory rather than raising output. Staff numbers fell from 299 at the end of 2012 to 88 in 2013. So much cash has been generated by reducing the extent of the business that the company was confident enough to hand back €36.3m to shareholders in December 2013. It still has €39.2m net cash. Now ‘restructuring is complete’ and ‘considerable progress was achieved during 2013 in lowering our wafer production costs, both internally and at our sub-contractors in Japan…our cash cost of wafer production is now closer to market prices…we are doubling our production output compared with 2013’. It currently operates at below 20% of its 750MW capacity. Globally, PV cell installation is rising by over 30% per year, giving hope that supply and demand will be better balanced in the future. It claims a positive EBIT for 2013 on continuing operations of €6.6m, but scepticism is required because €11.7m was added because of revised assumptions for onerous contract provisions. Also ‘The Board…does not expect the underlying business to return to profitability in 2014’. While profits are some way off, the company scores well on the other Piotroski factors. Piotroski factors (for 2013 prelims published in March 2014): 1. Profitable? Only in ‘continuing operations’ and only thanks to a provision releasea 2. Positive cash flow? Yes, after allowing for large decrease in inventory 3. Positive change in ROCE? Yes 4. Cash flow greater than profit? Yes 5. Positive change in debt to total assets ratio? No debt 6. Positive change in current ratio? Yes 7. Absence of equity raising? Yes 8. Trading margin improvement? Yes (lower loss) 9. Positive change in sales to total assets ratio? Yes In 2009 TEG group’s share price was 49p. It is now 4.5p with a market capitalisation of £8m. It scores well on Piotroski factors despite being unprofitable.

TEG is an organic waste technology company. It builds anaerobic digestion plants and in-vessel composting plants. Some plants produce gas to generate electricity which is fed into the grid and receives government incentives. Also vast amounts of compost is produced for sale. A new revenue avenue is being explored: piping gas into the gas grid. Selling heat is also possible. Local authorities are under pressure to recycle organic matter. If they send it to landfill they are charged £100 per tonne. They can sell it to TEG’s plants for £50-55 per tonne. Roughly half of the company’s revenue of around £22m comes from contracts to build plant for customers to then operate. This is a volatile source of income and has risks, e.g. Manchester Council have retained over £2m of the money they owe TEG for a plant until they are completely satisfied. The other source of income comes from running plant. For example, for the only AD biogas plant in London, commissioned and handed over in March 2014, TEG will receive £1.3m per year for 15 years. It also retains a 24.5% shareholding in the scheme (1.4MWs of electricity to power 2000 homes plus 36,000 tonnes pa in AD digestate plus 14,000 tonnes pa of compost for agricultural use). TEG operate over 10 plants around the UK. On the negative side (causing the share price fall) it made profits in only one year out of the last 10. Peter Gyllenhammer has built up a 20% stake, no doubt attracted by the high tangible net assets relative to market capitalisation. I guess he will be pushing for a greater focus on profits. The balance sheet seems strong, but is small considering that a plant can cost £10m-£15m. However, they usually partner with other organisation. In most years the absence of profits has meant that the directors have had to sell shares or raise loan capital to undertake projects. Tangible assets at June 2013 interims are £32.2m. Current liabilities of £13.3m and non-current liabilities of £2.2m leave £16.7m net tangible assets. Afarak Group is a company with a troubled stock market history. In the four years since it floated on the LSE its shares have drifted down from 160p to 32p. Thus it qualifies as a return reversal share. It also scores 8 out of 9 on Piotroski factors (at a pinch). Market capitalisation: £75m

Afarak owns chrome ore mines in South Africa, Turkey and Zimbabwe, and chrome processing facilities in South Africa, Germany and Turkey. Until five years ago it was a Finnish forestry and house building company. New directors with experience in chrome sold off the old assets and bought chrome assets. Subsequently it only made profits in one year (2011). The last dividend was in 2009. However the directors ‘firmly believe that ferrochrome will be in high demand in the long term’ and so are investing a great deal in more processing plant in South Africa with the expectation of ‘higher profit margin’ after Q3 of 2014. It currently digs out over 0.5m tonnes pa from a total estimated ‘ore resources’ of 61.3m tonnes. Capital expenditure in the year to Dec 2013 was €10.6m. Revenue: €135.5m (up 5.4% on 2012) EBIT: -€8m (better than 2012’s -€16.8m) Cashflow: €13.8m No dividend Piotrioski factors 1. Profits? No 2. Positive cash flow? Yes 3. Positive year-on-year ROCE? Yes, if you count profits being less negative 4. Cash flow greater than profit? Yes 5. Positive change in debt to total assets ratio? Yes (virtually no debt) 6. Positive year-on-year current ratio change? Yes 7. Absence of equity issuance in year? Yes 8. Positive change in profit margin over year? Yes, if you count that the loss is less 9. Positive change in sales to total assets ratio? Yes Buffet overpaid? I don’t think so

I have not yet read a proper analysis of Warren Buffett and Charlie Munger’s thinking in going for the Heinz deal. Here is my take. Imagine you are sitting there with billions of dollars. A deal comes along that offers a yield of almost 7 per cent. This comes about because you allocate $12bn in two ways: $8bn gets you 9 per cent yield (the preference shares) and $4bn gets you 2.8 per cent (the yield on the equity). Furthermore, that yield is likely to rise because the dividends on the equity portion will rise over time, as they have decade after decade. Not good enough for you yet? Perhaps you prefer Irish government bonds at 3.6 per cent, or gilts at 2.2 per cent. Or how about junk bonds at 6 per cent? Are these investments any more safe than a company with such a strong economic franchise that in all likelihood it will keep pumping out the dividends for decades to come. Now here is the icing on the cake. You also get 50 per cent of the equity in a company whose market power you have gazed at wide-eyed from afar since 1980. All that upside on top of a 7 per cent (and rising) yield. If that is overpaying then I’m a banana. In this case Berkshire Hathaway’s risk-reward position hinges on the preference share position, not on the price/earnings ratio of the equity position. 3G, on the other hand, has pure equity risk – and it is high. I do question the price they paid ($4bn for 50 per cent of the equity). They must be optimistic about boosting profits, I guess. I need help with this one. It has a market capitalisation of £7.7m and investment properties (long term lets) of £8.1m. In addition it has a portfolio of properties (something like two dozen sites) described as for ‘trading’. These are valued at the lower of cost or net realisable value, which is very significant as the open market value may be much more. The balance sheet values of the trading properties are £11.6m. Total liabilities are £3.2m. There are a few small items, leaving NAV at £16.9m and net current asset value at £8.8m. It seems to pass the first test of Benjamin Graham’s net current asset value investing.

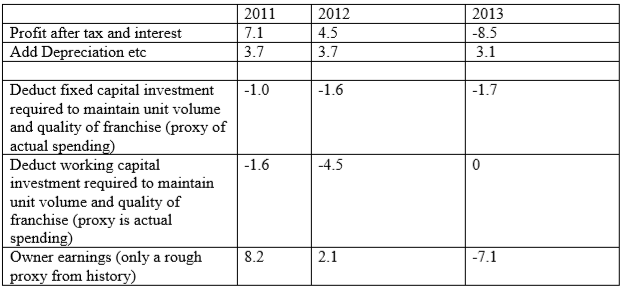

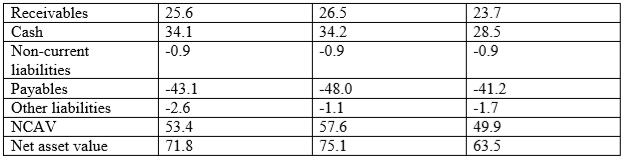

This reported balance sheet looks nice enough, but also consider the achievement of the management over the past five years. They might not have reported profit but they have created value by obtaining planning permissions on the properties. Here are some examples: -St Margaret’s House, Edinburgh. Currently 92,000 ft2 office building occupied by a charity on low rent and sublet to 250 artists. Parking spaces (120) let separately. In Sept 2011 permission was granted for 231,000ft2 of residential and/or student + hotel + offices + 225 parking spaces. -Brunston Home Farm, East Edinburgh. 3 Georgian Cottages for sale + consent to convert Georgian steading and reconstruct cottage + 10 houses + detached farmhouse + 2 acres of land -Belford Road, Edinburgh. Cul-de-sac 500m from Charlotte Sq and the West end of Princes St. Consent for 22,500 ft2 office + 14 car spaces or 20 flats + cars -Wallyford, Muselburgh. Building 5 detached + 4 terrace -Tamperion, Comrie. Smallholding. Consent for 12 detached houses -Chance Inn. Consent for 10 houses + upgrade of house -Strathray. 2 large detached + mansion -Fife. Cottage + 8 houses -Gartshare, 7 miles from central Glasgow. 120 acres of farmland, 80 acres of policies and tree-lined parks. Georgian pigeonnier + Victorian cottages and other buildings -Ardpatrick. ‘prospects for residential property extremely good’. Consent to change the use of ‘keepers’ and bothy. Being marketed. Plus ‘secluded sites – applying for planning’ -Shore Road. Consent for house + 2 others -Frithfield. Applying for 12 houses -Many other sites without planning permission. YET. As a property developer myself, I’m aware that it often makes sense to delay the realisation of value. This can create reported losses in the short run as you have to cover expenses with little cash coming in. Delay might be sensible because the depressed housing and/or commercial property market means that you will not cover your infrastructure costs, build costs and local authority demand costs. It might make sense because you want to modify the development plans to gain even greater value. Delay could also be wise if you anticipate that the property market will be much healthier two-three years down the line. Quotes related to this idea of delay: “Heavy infrastructure investment would result in an illiquid investment with very limited or nil profit margin. Accordingly, we continue to delay any major investment but to start, or prepare to start, on small low investment, low infrastructural projects.” (Chairman, 2012 annual report) “Unfortunately other potential new sites and many of the conversion sites are commercially difficult to realise. Current market conditions are unhelpful, but major continuing constraints are the high cost of conversion and the overall cost of upgrading the inadequate infrastructure, partially due to the required enhancement of the public services. Considerable effort has been expended on minimising the costs of reinstatement and development by operational efficiencies, but the current burdens and restrictions will curtail earlier plans, unless some relaxations become available or other development opportunities emerge.” (Chairman, 2012 annual report) Thus, for many of the sites it is not economically viable to build the properties which have planning permission due to high costs and an illiquid property market. This means that a valuation of the company hinges on the potential of the sites in a normal property market. There is good reason for hope: “Our development portfolio contains a very high proportion of sites with excellent planning consents, many of these gained in the last few years. Our several strategic land sites have been extensively promoted for inclusion in Local Plans and we have secured bridgeheads there. The investment in these long planning processes has been considerable and will be further reduced next year.” (Chairman, 2012 annual report) The only debt is £2.7m loan stock granted by Chairman’s other company. Interest is only 3% over base. Chairman has continued to roll over the debt for many years. Note the tax loses that have accumulated over the years. Quality of management Overall: Decades of experience in the property game plus high quality degrees plus a lot of skin in the game plus no sign (so far as I can tell) of poor sense of decency with respect to minority shareholders. The Chairman’s letters with the annual report show both awareness and analytical understanding of the macro and micro economic environment and a high degree of openness about the company’s strategy and individual projects. Douglas Lowe, Chairman and Chief Executive, Date of Birth 24/03/1937 Mr Lowe is a graduate of Clare College Cambridge University (MA Hons in Natural Science and Diploma in Agriculture) and Harvard Graduate School of Business Administration (MBA and Certificate in Advanced Agricultural Economics). Until 1977 he was Chief Executive of his family business, David Lowe and Sons of Musselburgh, property owners, farmers and market growers established in 1860, which farmed intensively 2,000 acres and employed over 200 people. In 1978 and 1979 Mr Lowe was Deputy Managing Director of Bruntons (Musselburgh) Limited, a listed company which manufactured mainly wire and wire rope and employed approximately 1,000 people. He was a significant shareholder and, from 1986 until shortly after joining the Company, Executive Deputy Chairman of Randsworth Trust PLC, a property company with a dealing facility on the Unlisted Securities Market. The market capitalisation of Randsworth Trust PLC increased from £886,000 to over £250 million between April 1986 and sale of the company in 1989. Mr Lowe purchased shares in the Caledonian Trust PLC in August 1987, at which time he became Chief Executive. Owns 78.47% of shares of the company. Michael J Baynham, Executive Director, Date of Birth 09/10/1956 Mr Baynham graduated in law (LLB Hons) from Aberdeen University in 1978. Prior to joining the Company in 1989, he worked as a solicitor in a private practice specialising in commercial property and corporate law. He was a founding partner of Orr MacQueen WS in 1981 and from 1987 to 1989 was an associate with Dundas & Wilson CS. Roderick J Pearson, FRICS, Non-Executive Director, Date of Birth 27/10/1954 Mr Pearson is a graduate of Queens' College Cambridge (MA Modern Languages and Land Economy) and is a Fellow of the Royal Institution of Chartered Surveyors. He has held senior positions in Ryden and Colliers International, practising in Edinburgh, Aberdeen and Glasgow, and now runs his own consultancy, RJ Pearson Property Consultants. The directors have complete control with 86% of the shares in their hands. Less than 1m shares are in free float (out of 11.9m), so these are very illiquid. Eight employees. Modest director remuneration: Total employees (with pension payments) cost under £0.5m. I D Lowe £142,000 and MJ Baynham £152,000 So the questions are: WHAT AM I MISSING? WHAT IS THE CATCH? Possible answers, if I was to play devil’s advocate and assume the worst: -As a minority shareholder you’ll never get a dividend, or you’ll get a paltry figure -The planning permissions are mostly worthless because the revenue from the completed schemes will not cover the costs, even over a five year horizon. This would call into question the capabilities of the directors and so would go against the evidence on knowledge and experience -The directors are simply not interested in generating wealth for minority shareholders. Any wealth produced will be siphoned off. To answer this one we need to know the characters of the main people. Can anyone help? -The economy and therefore the property market remains in the doldrums for the next 5-10 years. Caledonian keeps spending but the value declines. French Connection’s (FC) profit record is appalling. The only reason for looking at it is because it has net current assets much larger than market capitalisation and there are some reasons to believe that the assets will not be run down before profitability is restored. The fact that I put the probability of a return to health at less than 50% does not fatally wound the case for investment because if a turnaround is achieved the pay off will be 3-fold, 4-fold, 5-fold or more. An investment prospect with a less than 50% chance of success has to be taken only as part of a diversified portfolio, where, even if 60% of firms are failures, the few successes result in a satisfactory outcome. There are many negatives to weigh against the positives. I would be interested to hear how you weigh them. Investment category French Connection may fall into Benjamin Graham’s Net Current Asset Value style of value investing. This is: Shares that sell for less than the company’s net working capital alone. That is, the value of the current assets after deducting all liabilities, both current and long-term. Graham did take note of the possible market rationalisations justifying why companies sell for less than the value of their net working capital but frequently found them inadequate. In reality the negative factors were not of sufficient detriment to the financial strength of the company to justify pushing the share price so low – at least this was the case for the majority of shares within a portfolio of shares of this kind. He took current assets without placing any value on fixed assets, intangibles or goodwill, deducted all liabilities, and divided this by the number of shares, thereby giving a net current asset value (NCAV) per share. If this was more than the actual share price, then the company’s share was undervalued and therefore was a serious contender for investment. However, there is another stage of analysis: once a company passes muster on its quantitative elements, its qualitative elements are addressed, and an investor will then feel ready to invest. When a share selling for less than its NCAV is found the analyst should then check that its earnings are stable, its prospects are good given its strategic position and it has a good team of managers. At times of market downturns share buyers become fearful that there is worse to come; that a high proportion of quoted companies will fail to survive, waste resources in their struggle and then die, leaving the shareholders with nothing. This is exactly what happens to dozens of corporations. Graham accepted this but believed that a sufficient proportion of the shunned companies will regain value, so that buying a portfolio would be worthwhile. He believed that market pessimism can be indiscriminate. In the rush for the exit people dump shares for which there are good grounds for believing that recovery will eventually occur, as well as the real dogs. His reasons for expecting a revival of most of these companies: 1. Industries recover from downturns; in an overcrowded, over-supplied industry with low prices some companies do go under, leaving the survivors with a greater share of an improved market and higher profits. 2. Management can change their policies or be replaced, enabling their company to pursue a more profitable route. Managers in many of these poorly performing companies wake up and realise that they have to do better – after all their livelihoods are under threat. They switch to more efficient methods of production, introduce new products, abandon unprofitable lines. Sometimes shareholders need to apply pressure and force them to take a more commercial strategy focused on shareholder returns. The shareholders may replace the current team to do this. 3. Companies may be sold or taken over and their assets better used. 4. The management of a company selling below liquidation value must provide a frank justification to the shareholders for continuing. If a company is not worth more as a going concern then it is the shareholders’ interest to liquidate it. If it is worth more than its liquidating value then this should be communicated to the market. ............This qualitative analysis focuses on the following: Competitive position of the firm within its industry The operating characteristics of the company The character of management The outlook for the firm The outlook for the industry (from Great Investors (2011) FT Prentice Hall) See Testing Benjamin Graham’s Net Current Asset Value Strategy In London (2008) for a statistical analysis of the performance of investing in a portfolio of NCAV shares. Some data Share price: 30p Market capitalisation: £30m NCAV (as reported): £49.9m Revenue: -Approx. 70% UK/Europe (141 shops, 71 stores in UK and 46 concessions in UK and Europe). Operating profit: Retail lost £16m. Wholesale made £3.9m -25% N. America (17 shops) Op. Profit: Retail lost -£1.6m. Wholesale made £7.8m -Rest of world: wholesale made £0.5m op profit -Other income: UK £6.8m, NA £0.7m, RoW £1.6m Reasons for doubt In most NCAV firms you will find several reasons to want to hold your nose. Let’s look at those negatives for FC first: 1. Record No value generated for shareholders for a very long time. A story of decline. There are some businesses where management do not have to be smart every day because the franchise can carry them through years of poor management, (e.g. Coca Cola, Disney, Diageo). In retail you need to be smart every day because there is always a competitor with great innovation and flair snapping at your heels – especially in fashion retailing.   An owner earnings analysis does not make for comforting reading either:  2. Comments from many sources that they still have not yet got the pricing and store display right in the UK/Europe stores, even if there may be a glimmer of light on the styling. 3. Comments, unconfirmed, that the dominant shareholder (42%), founder, chairman and CEO is domineering and inflexible 4. Lease obligations amounting to over £200m, but spread out over many years. Should they be included in liabilities? (if so, how do we account for the assets these obligations provide?) 5. Even the Board are not anticipating a quick turnaround; aiming for breakeven in the year ending 31.1.15. 6. The brand is old and faded. Some positives 1. Cash at year end 31 January 2013: £34m, with no bank debt. January is a very advantageous point in the year to report net cash. However, even at the worst point net cash was reported as £10.6m during the year. Even better: in May 2013 it reported cash of £15.7m compared with £10.4m the previous year. Also no pension deficit. 2. NCAV   Bear in mind that Graham insisted that we reduce the reported receivables by one-fifth and the inventory by one-third of their reported value. Even with these deductions NCAV is significantly greater than market capitalisation. The question are: (a) Whether inventory is really worth what the company says it is? (b) Whether cash will be squandered?

2. While UK/Europe retail is doing very badly, the licensing and wholesale business continues to thrive (with a few bumps). Licensing alone can generate £5-£9m with few capital requirements 3. All it takes for the turnaround is good design. New head of design in May 2013 New head of Retail in Sept 2012. New head of production in October 2012 New head of multichannel October 2012 4. Asian growth: An aspirational brand in Asia, especially in China and India where operations are profitable and growing (opening 4 new stores in China this year and 10 in India). 5. Store leases in UK/Europe are likely to be for 15 years. This means that on average they have 7-8 years to run. Therefore over the next few years, store by store they can (a) stem losses by selectively not renewing leases (b) get rent reductions in a hard hit store rental market. The cash available combined with further reductions in working capital requirement releasing more cash, will see them through the next few years. Disposals in 2012/13: 2 stores in UK/Europe, 3 in N America. In process of closing one store and 6 concessions. Likely to close two more this year. About 10% of leases up for renegotiation each year 6. e-commerce is rising in importance, now 10% of sales 7. Sell in 30 countries with 1,000 stockists. Skilled weeding out of unprofitable activities still leaves much to build upon. 8. Branded sales (wholesale and licences for glasses etc.) of £400m, on which royalties are paid. Brand is still powerful in some segments/geographies 9. Trading revenue is now generally flat rather than falling, but such green shoots could wither. 10. Founder determination not to be seen as a failure in the retail game Some further thoughts A contribution to a bulletin board (ADVFN) posted 25.7.13 I have been reading the intelligent debate between PaulyPilot and CR with great interest. Thank you for bringing such thoughtfulness and expertise to the table. I have an idea that I think may help. As you’ll see I agree with both of you!! First let me start with an analogy: You go to the racecourse with two friends. One friend says that the positive points about a particular horse outweigh the negative the other says that the negative outweigh the positive. After listening to the debate you think that the chances of the horse being a winner are only 40%. Should you place a bet? Rationally that depends on the odds you are being offered. If you can get 5 to 1 odds then, even though the pessimistic person is more likely to be right, if you bet on many horses like this then over a period of time you will come out fine. Paul, with a great deal of industry knowledge, says that if the management do get their act together then this can be a multibagger. I agree, but that is a big ‘if’. If I do buy now, then in three years the chances (say 60%) are that I will look back and say that the company fell at a fence and I lost my money. Does that make it a bad investment decision? No. Benjamin Graham and Warren Buffett tell us that investment is not about getting every decision right in the sense that every one turns out a winner. You must factor in the odds as well. Thus if you purchase 10 shares in this category of Graham’s Net Current Asset Value shares over a period of years you will come out fine. You might like to see the evidence for such an assertion. As well as Benjamin Graham’s record you might like to look at an academic paper I wrote with Xiao Ying for The Journal of Investing ‘Testing Benjamin Graham’s Net Current Asset Value Strategy In London’ (2008). Being a statistical piece of work we were unable to filter out plain no-hopers or those with hidden liabilities (e.g. today we have Aga with its massive pension liabilities or Mallett with its shareholder wealth consuming managers and ‘value’ tied up in hard to value antiques) and yet, even with that constraint, the overall portfolio performance was very good over two decades. Don’t forget that Graham did not mechanically purchase all NCAV shares. He also examined for business prospects, stability and quality of management. Here we are on shaky ground with FC because we really do not know, we can only think probabilistically. But then with this investment category we are not doing a Warren & Charlie ‘Inevitable’ analysis in which we expect excellent management, economic franchise with a deep and dangerous moat and fantastic stability in every case (Warren might say we are picking up cigar butts though). We have to be prepared to take a chance on an individual share when it forms part of an outperforming portfolio. In the Benjamin Graham paper we did not manage to include an analysis of the proportion of shares that individually underperform within a high performing portfolio. However, in another paper examining return reversal we found that that only 47% of our ‘loser’ firms earn positive market-adjusted returns during the five years following portfolio formation. On average, 7% of losers are liquidated during the five test period years, leaving 46% that survive but under-perform the market. Despite this the loser portfolio outperformed the market by 8.9% per year on average – a minority of firms with very good returns dominate the performance (‘Financial statement analysis and the return reversal effect’ Working paper ) Graham thought that high NCAV firms might turnaround because of one of the following: (1) Earning power would be lifted to the point where it was commensurate with the company’s asset level. This could come about in two ways (a) a general improvement in the industry – entry and exit dynamics mean that low industry profitability is frequently not as persistent as many market pessimists believe , (b) a change in the company’s operating policies – management running a company with such a low stock price relative to assets either respond voluntarily to take corrective action or they (or their replacements) are forced to by stockholders, such as adopting more efficient methods or abandonment of unprofitable lines. (1) A sale or merger with another corporation that could employ the firm’s assets would take place. It would pay at least the liquidation value. (2) Complete or partial liquidation could release value. The management of a corporation selling at below liquidation value need to provide a frank justification for continuing to operate. In the case of FC I cannot see clearly the most likely reviving factor. I can say that exit from the industry by rivals is very unlikely to be valuable because there is also so much industry entry to keep pressure up. Liquidation will not release value because everything will be taken by the landlords. The main hope is a change in the quality of management. Are they now properly awake? Is the new talent really good? We will not know for some time – we can only play the odds. Please keeping put up evidence that might help us assess the quality of management. I hope this helps Glen |

Archive

I wrote newsletters for almost 10 years (2014 - 23) for publication on ADVFN. Here you can find old newsletters in full. I discussed investment decisions, basics of value investing and the strategies of legendary investors. Archives

October 2020

Categories |

RSS Feed

RSS Feed