|

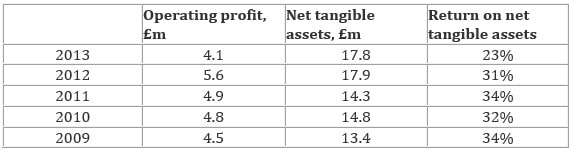

Dewhurst (LSE:DWHA) came out very well on my April 2014 analysis on its return on capital employed, which is a key indicator of ability to price products high relative to cost and therefore sign of a strong economic franchise. It also presents little to worry about in the balance sheet or in the Boardroom.  Return on tangible assets employed  With the company displaying a long history of high retention of earnings (low dividend payout ratio) put to good use in acquisitions and organic growth, generating returns on tangible assets of over 30%, there should be significant future growth in owner earnings to look forward to if this performance continues.

Balance sheet strength (based on 2013) Net asset value in total; £21.87m Net asset value per ‘A’ non-voting share: £2.57 Net tangible asset value in total: £17.86m Net tangible asset value per ‘A’ non-voting share: £2.10 Borrowing: zero Cash: £10.5m Pension deficit: £10.5m Character of the managers They have stuck to engineering, and with the exception of the mistake of the traffic management business (bollards, to put it politely!), they have focused exclusively on those areas where they have competitive advantage: lift components, keypads, train buttons, etc. However, they are now moving a little further away from the core by going for lift car manufacture and escalator belts. These moves are measured (£1m to £2m purchases every one or two years) and they are still reasonably well related to the core. They tell it like it is. No embellishment, frequently subsequent events show them to have been overly pessimist. Smart in assessing value in forms other than in engineering. For example, they recognised that the value of the factory in Hounslow would be worth considerably more if they obtained planning permission to build houses and then sold the land. It was sold for £6m in cash (£5m plus £1m of VAT) and then they paid a special dividend. The family own over 50% of the voting shares and have consistently demonstrated that they run the business as ‘if they are the sole asset of their families and will remain so for the next century’ (Buffett 1999), with steady growth within their circle of competence, constant bearing down on costs, high quality interaction with long-term customers, conservative investment and borrowing policies. Bulletin Board comments on the character of the managers are overwhelmingly positive. They are highly respected with long track record of treating shareholders well. They have carefully nurtured a family business in which they take great pride. Richard Dewhurst (Chairman) has an engineering degree and an accounting qualification. He has worked at Ford and as a management consultant. David Dewhurst, MD, has an engineering degree and previously worked at a brand design consultancy. Total director emoluments in 2013 were £654,000, with the highest paid director receiving £189,000. Richard Dewhurst bought 2,000 Non-voters in October 2013 at £2.849. The next Newsletter will outline an industry analysis and an extraordinary resource search analysis

0 Comments

Leave a Reply. |

Archive

I wrote newsletters for almost 10 years (2014 - 23) for publication on ADVFN. Here you can find old newsletters in full. I discussed investment decisions, basics of value investing and the strategies of legendary investors. Archives

October 2020

Categories |

RSS Feed

RSS Feed