|

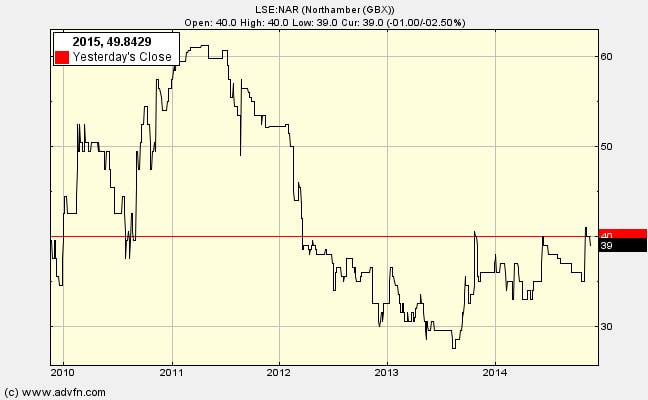

Before selecting Northamber for the 2013 portfolio I worried about its business environment and wondered how the value tied up in its net current assets could be released. Here is what I wrote in August 2013 (it has a bearing on the November 2014 decision):  The fly in the ointment

Northamber trades in an industry with some of the worst economic characteristics I have come across. It is a medium sized player in an industry in which entry is wide open (there is little customer captivity/loyalty). Suppliers hold a great deal of power. Customers can quickly obtain alternative prices from competing wholesalers. Substitute methods of getting the product (e.g. computer) to the end-user are viable (e.g. manufacturer selling direct). Furthermore, the year on year product price falls and manufacturers on wafer thin margins expect wholesalers to also operate with low gross profits (in Northamber’s case 7.7%). So what can save this company from cash burn and continuous slide? NCAV shares have serious problems but they usually improve their positions in one or more of the following ways: (1) Industry economics change as result of competitors exiting the industry. The last man (men) standing gains in pricing power to return to reasonable profitability. This is possible with Northamber, but unlikely. It will be one of last standing because of its strong BS and its ability to reduce overheads as sales fall to remain close to breakeven, but I cannot rely on there being a sufficient number of competitors exiting to make a material difference to profitability. There is a good chance that new competitors will emerge. (2) Earnings power will be lifted. Management will stop the slide by returning the company to fair ROCE through excellence in operations or by stopping the head-against-brick-wall-banging and reallocating assets to areas of business with better returns. Here we have some hope. The senior team are very experienced and have shown a willingness to drop low margin products. (3) Liquidation. This is a possibility. It seems to be happening to some degree by stealth: Over the past 6 years turnover has declined from around £200m to around £80m, and with that there has been the release of cash from working capital and quite high dividends and share buy backs. (4) Takeover. Perhaps another industry player will bid for it, but how valuable is the client list when buyer switching cost is so low. The next blog will tackle managerial quality and commitment, and pose some critical questions about this business.

0 Comments

Leave a Reply. |

Archive

I wrote newsletters for almost 10 years (2014 - 23) for publication on ADVFN. Here you can find old newsletters in full. I discussed investment decisions, basics of value investing and the strategies of legendary investors. Archives

October 2020

Categories |

RSS Feed

RSS Feed