|

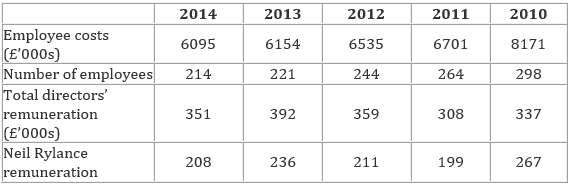

Airea has been purchased as a net current asset value share. This means that it must score reasonably well on a qualitative analysis of its business prospects, management and stability. Overall, it comes out well.  Prospects for the business Carpet sales, particularly those for offices, schools, etc., are particular vulnerable to an economic downturn. Through the Great Recession Airea lost sales, but remained profitable. This demonstrates some resilience. It also indicates that the competition is not as cut-throat as it is in some other industries. Or, at least, it has not been too margin-damaging in the past; whether, in the future, competitors will pressurise more on price remains a possibility. Can anyone reading this help us make an assessment here? If carpets are a strongly cyclical then 2015 might be seen in retrospect as the year when sales, profits and owner earnings took off. Up to June 2014 no take-off was detected, with the directors talking of ‘the long awaited recovery in the residential carpet market still awaited’. Quality of managers They have certainly been tested in a harsh environment. Neil Rylance joined the company (Sirdar) as MD of floor coverings in 2008 and shortly afterwards became CEO of Airea. Talk about baptism of fire! He had to deal with the Sirdar legacy and a large decline in demand. But, he had faith – he bought 5.43% of the shares. Martin Toogood joined as an independent NED and he too put his money where his mouth is by buying 4.54% of the shares, mostly at prices higher than today. He is now Chairman. Roger Salt joined in 2004 became Company Secretary in 2009 and FD in 2011. He has a relatively small shareholding. Is that a negative indicator? A case can be made arguing that there is some degree of alignment of managers’ and shareholders’ interests given the share stakes held by the two main leaders. While 45% of the share capital is in ‘non-public’ hands, most of this is held outside of the current Board and so the current managerial team must feel some vulnerability to being replaced if they prove unsatisfactory. These highly experienced managers are not prone to over-optimistic statements on the prospects for the business as you can see by reading the annual reports. While they hope for recovery they anticipate that ‘competition will remain fierce’ and that in the meantime they concentrate on product innovation and efficiency gains in operations: ‘the cost base remains constantly under review.’ A glimpse of that focus on efficiency is provided by the employee statistics, with a gradual lowering of employee costs and flat-lining of director’s remuneration. Employee statistics  Stability of the business

First, with no debt and £2m on hand there is no financial gearing risk. Second, with profits shown through a recession the indications are that the underlying operating business is stable. But this could change in the blink of an eye of a competitor’s strategy meeting. But would a price war suit any of the carpet suppliers? Third, the managers seem to want to stick to their knitting, concentrating on the business within their circle of competence rather than experimenting. Fourth, the pension deficit is volatile and could conceivably crush the business given the size of the liability (over £40m) relative to the MCap of the firm (£5.41m) and the value of net current assets (£5.465m). Fifth, if the worst of the economic cycle is behind us, then stability could improve as the BS is strengthened further and the pension deficit is eliminated. Tomorrow's blog raises the questions we need to keep asking

0 Comments

Leave a Reply. |

Archive

I wrote newsletters for almost 10 years (2014 - 23) for publication on ADVFN. Here you can find old newsletters in full. I discussed investment decisions, basics of value investing and the strategies of legendary investors. Archives

October 2020

Categories |

RSS Feed

RSS Feed