|

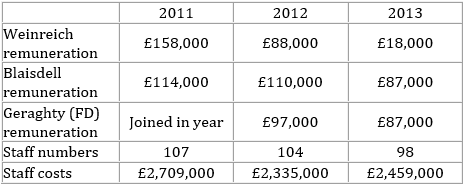

Holders Tech may have a strong balance sheet, a multiple of net asset over its market price, but does it have potential to create shareholder value through its operations or its liquidation? To arrive at a judgement we need to consider the management, the firm's business prospects and its stability:  Managerial competence and integrity. On the positive side, the two key people have spent a large part of their adult lives working for this company. Rudi Weinreich (68) founded the company in 1972. He is Executive Chairman with 47% of the shares. He has strong incentives to revive the company from its moribund state. First his financial stake could rise in value, or at least the flow of dividends could increase. Second, this is something he created – surely he will want to create a better legacy than this? Victoria Blaisdell (42), Managing Director, joined in 2004 (shareholding 0.81%). The UK head joined 1996, German joint heads joined in 1993 and 2002. Judging by their statements, they are realistic and transparent about the difficulties of distributing products into these markets. In terms of integrity regarding small shareholders they have taken personal hits on remuneration over the last three years:  Thus there has been some alignment of shareholder returns and managerial returns.

There is a wider push on administration costs: “Total administrative expenses were reduced by £226,000 compared with 2012 so that administrative cost as a proportion of revenue decreased from 24% in 2012 to 21.4% in 2013” (2013 report) A very low level of capital expenditure – around £100,000 pa. They also continued to pay a dividend. But you have to be concerned that they have not found a way to consistently sell product above cost. Perhaps a good excuse is that the recession in Europe has depressed the more recent profit picture, but I might be clutching at straws. No independent directors Stability It is stable alright – no debt, virtually no pension deficit, turnover stable, assets to fall back on, stick to their knitting – but it is stable at a low level of profits over a span of years. Business prospects This is very cloudy because time and again in the past the managers have claimed that matters are improving and then the following year they report ‘strong competition’ and ‘over capacity’. Admittedly, some of the problems were due to the Chinese business draining financial and managerial resources. Now that has been disposed of they might be able to concentrate on finding a profitable niche. However, this quote from Ben Graham brings some comfort, as it makes clear that when you have a high margin of safety in NCAV and NAV, you do not need outstanding business prospects: “The buyer of bargain issues places particular emphasis on the ability of the investment to withstand adverse developments. For in most such cases he has no real enthusiasm about the company’s prospects. True, if the prospects are definitely bad the investor will prefer to avoid the security no matter how low the price. But the field of undervalued issues is drawn from the many concerns – perhaps a majority of the total - for which the future appears neither distinctly promising nor distinctly unpromising.” The next blog will conclude my analysis of Holder's Tech.

0 Comments

Leave a Reply. |

Archive

I wrote newsletters for almost 10 years (2014 - 23) for publication on ADVFN. Here you can find old newsletters in full. I discussed investment decisions, basics of value investing and the strategies of legendary investors. Archives

October 2020

Categories |

RSS Feed

RSS Feed