|

Investors need stock brokers to deal for them. But with so many options when choosing a stock broker. An investor often finds himself lost or even scared.

There is absolutely no reason to be in awe of stockbrokers, nor of the process of buying or selling shares. Stockbrokers need you more than you need them. It is a highly competitive business, with dozens of brokers offering to help you make a transaction – so much so that you can now deal for less than £10. Choosing a broker means selecting the right combination of cost and services. The following selection criteria may help you draw up a shortlist of brokers and make a final selection: Charges. Of course, the lower the commissions for trading the better, but you should allow for the possibility of improved service at extra cost. An important aspect of improved service is the effort put into ‘price improvement’ which is taking action to obtain better prices than the current bid and offer prices shown on the screens, through, say, haggling with a market maker. The charging structure will make a big difference to your choice of broker. For example, an investor who does not want to pay for advice and trades many times each month with bargain sizes of around £5,000 will prefer a broker who charges a low fixed rate regardless of bargain size, say £20 each time. Another trader, who buys and sells £1,000 of shares, may prefer a broker who charges a percentage of the amount of the trade, say, 1.0 per cent. If you are a buy-and-hold investor, with few transactions, commission costs will not be a great concern. But if you are very active the charges mount up dramatically. Then you may opt for the cheapest mode of transacting – usually online. This might be fine for the most liquid shares with narrow bid-offer spreads, but for infrequently traded shares the bid offer spread can be 10% or more and a telephone service broker might be able to negotiate a better price. Location. The possibility of being able to talk to a broker face-to face may lead investors to favour a local broker. This can be particularly valuable for discretionary and advisory portfolio management, where the broker needs to know the investor’s circumstances and investing objectives. Local brokers may also be knowledgeable about companies in the region. Contact. In surveys investors usually place the ability to contact brokers at the top of their worry list. There are many complaints about telephone lines being busy when a client wishes to deal. People can be put on hold for 20 minutes or more. This can seem like an eternity when you are trying to sell and the market is falling like a stone. Brokers are also criticised for not calling back when they promised to do so. Online orders are often executed very slowly at busy times, as the IT systems suffer from overload. Unfortunately, this is one of those factors that you do not really find out about until you experience it. However, it might be worth asking other clients of your shortlisted brokers if they have any complaints. It could be useful to be able to switch totelephone dealing if the online system is down, and vice versa. So consider a broker that gives you this flexibility. Administration. The second factor most complained about is the quality of the administration. Record keeping is sometimes poor, as is the administration of dividends and taxation matters. The paperwork may reach the investor weeks after the event. You do not have to put up with this: other brokers are highly praised for the speed and efficiency of their administration. Expertise. You need a broker who is well resourced, has access to high-quality external data and attracts talented managers. This is especially important if you are asking for portfolio management services. You do not want your nest egg managed by a graduate trainee trying to learn on the job. Ask what experience the firm has in managing portfolios of the type and size you have in mind. Performance. Unfortunately, independently constructed league tables of portfolio managers’ performance are not available and so comparison is all but impossible. Brokers do provide statistics, but you must view them with caution.2 Recommendation may be your main hope. Interest. Brokers hold money in cash accounts on behalf of investors. Some of these accounts offer miserly rates of interest, if anything. Those If you are likely to depositing substantial sums with a broker you need to ask what rate of interest you will be received prior to the purchase of shares. Also, if you need temporary credit, what limit will the broker allow you to go up to? Adapted from the book: Financial Times Guide to Investing

0 Comments

Mohamed El-Erian, formerly CEO of PIMCO bond investors, IMF Deputy Director economist and chair of President Obama’s Global Development Council, is lauded for his clear thinking on financial and economic affairs. In the last two weeks he has granted interviews to discuss the crisis. Here are the highlights.

Economic stops are worse than financial stops “Economic stops [as opposed to financial stops] sneak up on you. They reach critical mass before you realise what is going on. And then dealing with the underlying source is very difficult. In this case it’s a health issue.” “Economic sudden stops are very unfamiliar to people who haven’t lived in fragile and failed states, who have not gone through a big natural disaster. They bring everything to a halt. They destroy supply and demand simultaneously. It starts small (China) but it spreads, and it reaches critical mass which is what has happened in the global economy.” Dealing with sudden economic stops “Stimulus policies do not work. No matter what tax break you give to people; no matter how cheap their loans are; no matter how much cash is in their pockets, this will not let them go out and spend. They will wait. You can help with the balance sheet, but, unfortunately, you cannot reactivate economic activity until your health issue is addressed”. “The only way you can contain and counter this virus is by denying it the oxygen it needs to spread – people’s contact. People put health before anything else. In California, well before we were mandated to stay at home, my hair cutter said, ‘I’m staying home’. Why? ‘I’m scared’. I asked: ‘but what about your business?’ Answer: ‘I put my health ahead of my income.’” “Fiscal policy can help people through the sudden stop, support their balance sheets, make sure they can afford payments, or press pause on certain payments, make sure liquidity problems don’t turn into solvency issues.” After yesterday’s announcement from the Fed that it would buy junk bonds yesterday: “one of the concerns the market had is that we would have a massive round of downgrades – it has already started – and that companies would thereby lose the indirect support of the Fed. What the Fed has said today is: No, I am going to take a snapshot of where the economy was, I want to make sure than liquidity problems don’t become solvency problems, and therefore I will not penalise companies that were downgraded because of liquidity issues. That is a very clear statement, it’s a very strong statement.” Thus some highly indebted large US companies are to be saved. A market ripe for falling “In 2019, despite sluggish economic and corporate fundamentals, the S&P 500 was up 30%. More risky assets were up even more. At the very same time that that happened you also made money on government bonds. So, you made money on the risky stuff, and you made money on the risk-free stuff. That is not supposed to happen. And at the same time volatility was very very low. What that tells you is that the marketplace had been conditioned to care about only one thing to the exclusion of all else, and that is central bank liquidity. Particularly the predictable and ample injection of central bank liquidity The result is a market that underappreciated liquidity risk, credit risk and equity risk. And we now, unfortunately, are reversing all three.” “Every single segment in the economy, except for a handful, will go through the demand and supply destruction that the airline industry has gone through.” Has the market fallen enough yet? “I’m pushing back against this notion that we have established a bottom. It’s a counter-trend rally. We are still on a downward trend.” “Most people haven’t priced in the unc ………………To read more subscribe to my premium newsletter Deep Value Shares – click here http://newsletters.advfn.com/deepvalueshares/subscribe-1 Professor Nouriel Roubini, economic consultant and teacher at New York University's Stern School of Business (formerly IMF, World Bank, President Clinton’s senior economist) is renowned for warning of impending disaster prior to the 2008 financial crisis. He has long been a student of emerging market crashes, and this knowledge helped him spot the looming disaster in the U.S. 12 years ago, "I've been studying emerging markets for 20 years, and saw the same signs in the U.S. that I saw in them, which was that we were in a massive credit bubble,"

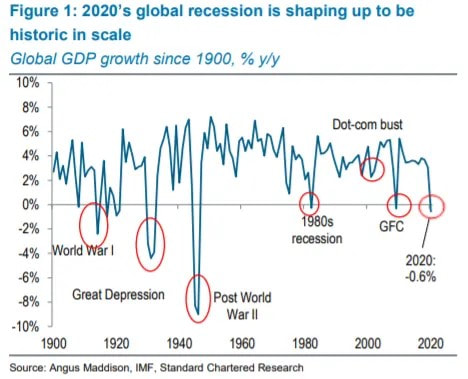

He has been speaking out in a series of interviews and an article in the last two weeks. Here are some of his ideas. He quoted some Goldman Sachs and JP Morgan research indicating that US output will fall at an annualised 25% rate in the second quarter, “worse than the Great Depression because the freefall in output occurred not in three years but in three weeks. Everything is in freefall. We are now on the verge of something that could be worse than the Great Financial Crisis. We could get into another Great Depression.” Despite central banks doing the right thing in supplying money “with half a million cases of COVID-19 we are not going to be able to reopen economic activity. If the contagion is not stopped then we’ll have the conditions for a Depression, not a recession.” In the Great Depression (GD) and the Global Financial Crisis (GFC) stock markets collapsed by 50% or more, credit markets froze up, massive bankruptcies followed, unemployment rates soared above 10%, and GDP contracted at an annualized rate of 10% or more. “Already US Treasury Secretary Steve Mnuchin has warned that the unemployment rate could skyrocket to above 20% (twice the peak level during the GFC). Every component of aggregate demand – consumption, capital spending, exports – is in unprecedented free fall.” He dismisses self-serving commentators who have promoted the notion of a V-shaped downturn – with output falling sharply for one quarter and then rapidly recovering the next, “it should now be clear that the COVID-19 crisis is something else entirely. The contraction that is now underway looks to be neither V- nor U- nor L-shaped (a sharp downturn followed by stagnation). Rather, it looks like an I: a vertical line representing financial markets and the real economy plummeting.” Never before has economic activity just shutdown like it has now, not even in the GD or the GFC. The best he can hope for is a downturn that is shorter-lived than in the GFC but it will still be more severe. “This would allow for a return to positive growth by the fourth quarter of this year. In that case, markets would start to recover when the light at the end of the tunnel appears”. But this depends on several things going right:

In China some shutdown measures have already been eased. Does that mean its economy will rebound to the a priori position soon? If so, then perhaps westerners can stop worrying about deep recession because all we need to do it copy the Chinese anti-Covid programme and get going again.

Other models to follow are Singapore, South Korea, Japan and Hong Kong which have done a relatively good job of containing the virus. Does this mean that their economies will suffer little damage and get back to normal soon? Today I’ll look at how these countries are faring. China There is some good news to report: the official rate of infections has slowed dramatically, as has the death rate – see chart. China went through a period when it was operating at only 60% of normal economic output. Since then GDP has risen as reflected in purchasing managers indices, which indicate that there are more factories and service companies open for business in March than in February. We can see the improvement in some statistics. For example, congestion in major cities is now only 25% down on its 2019 rather than the 60% drop in February. But note: people may be more willing to get in their cars, but they are still very reluctant to ride the subways, which are down 50% on normal, despite government shutdowns being eased and the Communist Party desperately encouraging people to return to work. Also families will still not mix with others in cinemas. And they are buying 25% less property than they did in a typical day in 2019. Heat and electricity are still required in households, but overall demand for coal is still significantly less than in 2019, presumably because many factories are drawing electricity from the grid. Economic activity, as proxied by intensity of light in industrial parks, is still around 25% down on 2019. We can conclude from the above, firstly, that China is nowhere near back to normal, and second, that it is looking its first recession since 1976. “The real unemployment rate in China is likely to go higher than 10% for sure,” said Diana Choyleva, chief economist at Enodo Economics in London. “Q2 [economic activity] is shaping up to be very weak as disruptions to production in China linger and, more importantly, demand from the rest of the world evaporates.” Last week a team of ANZ economists projected that China’s first quarter GDP would fall 9.4% YoY, with another annual decline up to 2.1% possible for the second quarter. But China have opened up Wuhan and other Coroaavirus hotspots haven’t they? So it’ll get back to normal soon, surely? The prospect of China getting rid of restrictions Yesterday, health authorities reported 62 new coronavirus cases (in Shandong and Guangdong). As a result of regular out-breaks China has imposed strict rules on who can enter the country and enforces quarantine measures in a bid to prevent a wave of imported infections. When relaxation of lockdown occurs people fear a second wave of infections as exemplified by Wuhan’s lifting its official ban on travel today, “But for many of Wuhan’s 11m residents, the formal lifting of restrictions on movement is just the start of a long recovery for a city in severe economic distress and a population fearful of a second outbreak. Activity has picked up on the streets of Wuhan but many businesses remain shut. Scores of residential districts around the city are still sealed off, barring free movement. Many people ………………To read more subscribe to my premium newsletter Deep Value Shares – click here http://newsletters.advfn.com/deepvalueshares/subscribe-1 First the International Monetary Fund: Paul M. Thomsen of the IMF wrote last week that the service sectors closed in Europe and North America generally account for one-third of national output. This loss translates into a 3% drop in GDP per month while these sectors are out of action.

I’m going to make an optimist assumption now. After three months of lockdown all the major economies will be back to normal with everyone who wants to work working again and companies pumping out just as many goods and services in a typical day as they did in 2019. With this assumption the loss in GDP is of the order of 9% for 2020 as a whole. That is, this year the people of, say, the UK produce 91% of what they produced in 2019. For this rosy scenario to work out people need to be convinced that the risk to them or a member of their family of dying of Coronavirus is negligible – they won’t catch it on the Underground, nor in the office or pub. On top of that it assumes that the vast majority of companies survive the crisis period and can quickly get back to full speed and employ as many people as they did before. But there will be complications Just to give you one example of the grit likely to be in the machinery after three months of lockdown I could look at shopping centres. Currently the owners of these buildings are, on average, receiving only one-third of the rents they are due; most retailers are simply refusing to hand over the cash. Many of these landlords have high debts to serve (e.g. Intu has £4.5bn and has already breached covenants with its bankers). Many analysts think vacancy rates in shopping centres and the high street could double to one in five in the coming months even if the government gave the all-clear. There will be many retailers and many property companies going bust. There will be associated employees and former employees exhibiting much more restrained spending patterns post-virus. Another example: fashion suppliers to the major retailers are receiving letters telling them that spring/summer orders will not be paid for (or that they will extend payment terms). This will destroy firms and factories all the way down the supply chain. Furthermore, many of the retailers will also go bust in the next few months, often affecting a long line of creditors (similar stories are likely in many supply chains, including those for restaurants, pubs, hotels and airlines, each with powerful knock-on effects) A less optimistic picture Looking at the epidemiological work and clear absence of proven antivirals and anti-inflammatories, let alone widespread testing or a vaccine, it seems far more likely that the lockdown or at least a squeeze-and-let-go semi-lockdown will still be in place in the autumn. If 3% of annual GDP is lost for each month of social distancing and governments do not lift restriction for six months we end up with and loss of 18% of GDP in 2020 compared with 2019. And that is before other disruptions and spillovers to the rest of the economy are taken into account. “A deep recession this year is a foregone conclusion” writes Paul M. Thomsen. He is backed up by the World Bank: “We expect a major global recession”. Already one-fifth of all French private sector employees (in 400,000 companies) are seeking temporary unemployment benefit. That is 4 million people. In the UK one million signed up for Universal Credit last week, during which time 6.6m Americans sought unemployment relief, taking the total number of Americans filing a new claim for unemployment benefits in the two weeks ending March 28 to 10 million (and many states are yet to shutdown; when they do unemployed numbers will rise). In addition to registered unemployed about half of the UK workforce is on furlough and millions of self-employed are idle. Organisation for Economic Cooperation and Development, OECD In country after country spending has been ………………To read more subscribe to my premium newsletter Deep Value Shares – click here http://newsletters.advfn.com/deepvalueshares/subscribe-1  Our lives are going to be shaped by the coronavirus, not just our health, work, relationships, politics and social interaction but, of more direct relevance to an investment newsletter, economies, businesses and shares. If we are about to enter a depression as deep and widespread as the one in the 1930s hundreds of millions of people will suffer and millions will die, not just directly because of the virus but from the knock-on economic effects: starvation and poor access to basic medical care as dislocation lowers production and destroys the political and business order in poor countries and in pockets of “rich countries”.

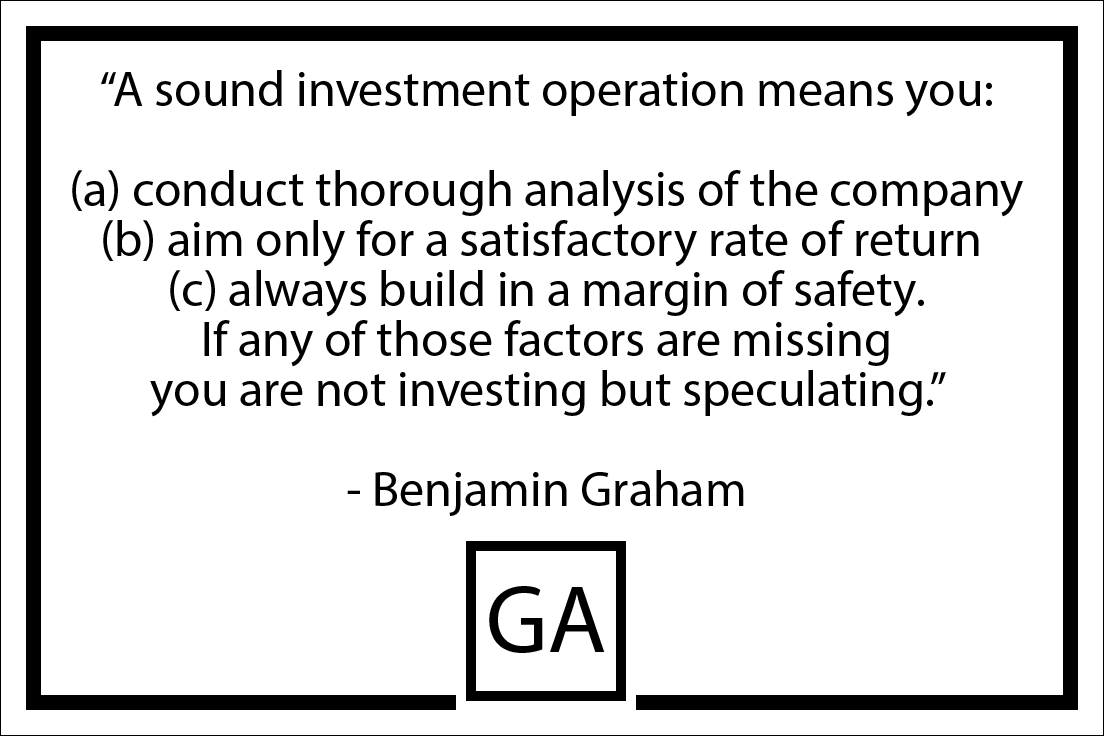

Expect foodbank queues to be as long as those of the soup kitchens of the 1930s. Expect personal bankruptcies, domestic violence and suicides to rise. Businesses will fail by the tens of thousands, large and small, and stock markets will fall dramatically from where they are now in over one hundred countries. And these effects will be played out over years, with many false dawns, and more violent downward shifts. There will be a strung-out deficit in consumer demand at the macro-economic level, as people become increasing afraid to buy for consumption, or to buy investment items. If that is the most likely outcome we need to position our personal finances and our portfolios to reduce the potential for regret, to hedge the downside, to have cash at hand to both weather the storm and to take advantage when green shoots come through. Some very able analysts are saying that another Great Depression might very well occur given the public health and fiscal errors made so far in fighting the virus. One even goes so far as to say it could be a “Greater Depression”. In future newsletters this week we’ll look at some arguments for and against. The Great Depression In the 1930s real output of the US economy shrank by 30% and unemployment went to 23%. It wasn’t quite so bad in the UK with 20% unemployment, but in Germany hyperinflation reigned as well as 30% unemployment – and we know the political consequences of Germany’s economic travails. Worldwide GDP fell by an estimated 15% (compared with 1% in the so-called Great Recession of 2008-10). International trade halved and construction virtually halted. There is no agreed definition of a depression other than saying it is a severe and sustained downturn. For our purposes I’ll use a decrease of GDP greater than 15% as a benchmark. A deep recession A deep recession is not much to celebrate, but it is perhaps the best we can hope for. It will result in the quantity of goods and services being produced in Europe and North America and many other countries being reduced by at least 6% and quite possibly by over 10% compared with the amount in 2019. That is just the first-order effect. To consider the second-order effects transport your thoughts forward 12 months from now and consider what you might have experienced. If you are British you might have s ………………To read more subscribe to my premium newsletter Deep Value Shares – click here http://newsletters.advfn.com/deepvalueshares/subscribe-1  Benjamin Graham, Warren Buffett's mentor ran a fund with assets under management of £2.5m in 1929. The crash wiped out most of that. In the Depression he pondered the meaning of "investing" as opposed to "speculation" and wrote the very influential Security Analysis book. Warren Buffett became his student in 1950. After regaining his investors' money, between 1936 and 1956 Graham achieved average annual returns of 20%.

A sound investment operation means you (a) conduct thorough analysis of the company (b) aim only for a satisfactory rate of return (c) always build in a margin of safety. If any of those factors are missing you are not investing but speculating (e.g. buying on tips or inside information ignoring analysis, trying to guess short term market moves). He realised he had been speculating prior to the Crash. The searing experience of the Crash led to the foundational value investing philosophy he developed in the 1930s. |

Glen ArnoldI'm a full-time investor running my portfolio. I invest other people's money into the same shares I hold under the Managed Portfolio Service at Henry Spain. Each of my client's individual accounts is invested in roughly the same proportions as my "Model Portfolio" for which we charge 1.2% + VAT per year. If you would like to join us contact Jackie.Tran@henryspain.co.uk investing is about making the right decisions, not many decisions.

Categories

All

Archives

May 2023

|

RSS Feed

RSS Feed